2026 State of the Pre-Roll Market Report

Posted by Custom Cones USA on Apr 14th 2026

Executive Summary

While the broader U.S. cannabis market slowed to 1.5% growth in 2025, one category continued to expand at a pace more than six times faster: pre-rolls.

Pre-roll revenue grew 9.8% year-over-year with unit sales increasing 18.6%, the strongest revenue and unit growth of any major category in cannabis. And perhaps more significantly, for the first time in the history of the legal cannabis industry, pre-rolls outsold every other product category by units.

In a maturing market defined by price compression and margin pressure, pre-rolls have emerged as not just a reliable segment, but as the driver of growth for the entire industry.

Drawing on sales performance data, product-level trends, SKU analysis and feedback from more than 125 companies representing every corner of the pre roll industry, this report examines the data behind that shift and looks forward to the trends that will define the future of pre-rolls, including:

- the continuing shift toward infused and premium products;

- the dominance of multi-pack formats;

- the branding strategies that keep the leaders at the top of the sales charts; and

- emerging opportunities for growth in an increasingly competitive marketplace.

2025 Pre-Rolls Statistics

Pre-rolled joints have been part of the legal cannabis industry since its inception, a consumer packaged goods version of the classic hand-rolled joint that has become a symbol of the industry itself.

But for the entire history of legal sales, flower has remained king, with every other category measured against its dominance. Until 2025.

This past year, for the first time, pre-rolls outsold every other category – including flower – in terms of units sold. That’s something that would have seemed crazy just five years ago when the legal markets opened and pre-rolls were something of an afterthought or way for producers to make a little extra profit on trim or shake, a convenience product positioned at the low end of the price spectrum.

But no more. Pre-rolls have consistently outperformed the rest of the cannabis industry with five years of continuous growth, becoming the primary driver for the entire industry and the most innovative and dynamic product form on the market. They’ve even taken over the top category in Canada.

Today, after five years of continuous expansion, pre-rolls are the biggest drivers of growth in the entire industry. Not only do pre-rolls sell more units than any other category in the U.S., but it saw the largest growth in the industry in 2025 in terms of revenues and units sold, raking in nearly $3.6 billion for a 15.9% market share, up 7.6% year-over-year.

This report looks deeper at what pre-roll products, brands and trends are driving the category’s accelerated growth, as well as where we see it going in the future.

About This Report

The analysis here is drawn from comprehensive point-of-sale data, new product launch data and SKU-level performance metrics from 15 states, collected in 2025 by cannabis analytics firm Headset. The objective is to take a data-driven look past the surface numbers to analyze the dynamics, competitive patterns and opportunities that will continue to define the category.

That data, combined with survey responses from more than 125 companies from every corner of the pre-roll sector, is designed to give a glimpse into this important and growing category, as well as provide insight for those looking to scale or expand their pre-roll brands as the market expands.

Table of Contents

By the Numbers |

State Markets |

Segments |

Pricing |

Brand Performance |

Multi-Packs

Consumers |

New Products |

Opportunities |

Predictions |

Brands Surveyed |

Production

Pre-Roll Types |

Infusion |

Machinery Used |

Bottlenecks |

What Consumers Care About |

What’s Next

Pre-Rolls by the Numbers

Let’s begin with a detailed look into the Headset data to get a more complete and well-rounded picture of the pre-roll category compared to the broader cannabis market.

2025 Pre-Roll Sales and Market Share

Key Stats

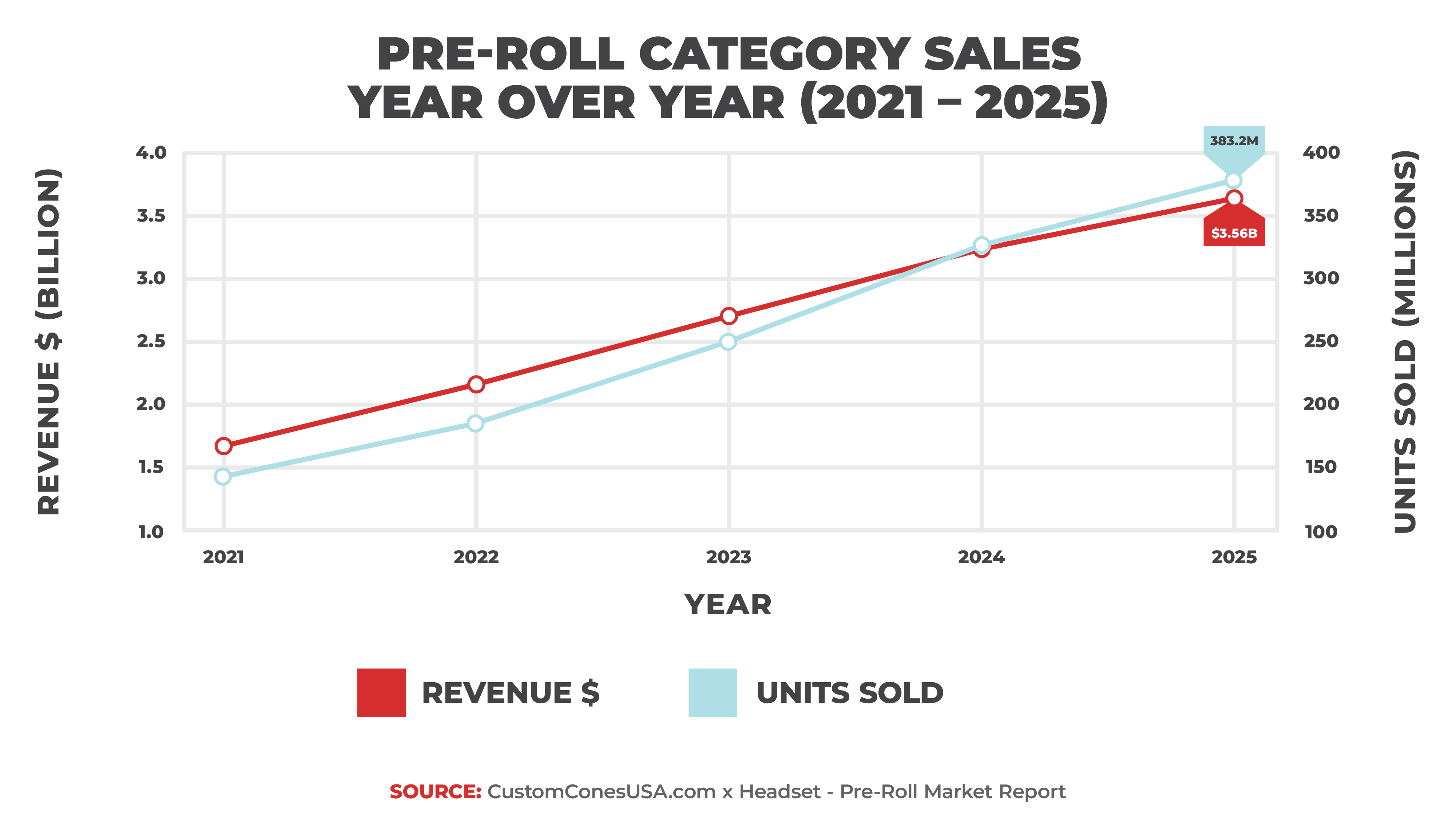

- $3.6B in pre-roll sales in 2025, representing a 15.9% market share and 383.2M units sold

- +9.8% revenue and +18.6% unit growth, outperforming total market growth of +1.5%

- Revenue has more than doubled since 2021, growing from $1.68B to $3.6B

- Market share increased 29.5% over five years and 7.6% year over year

2025 marked the biggest year ever for pre-roll sales, raking in nearly $3.6 billion in sales and moving 383.2 million units. That’s a 9.8% growth in revenues and an 18.6% growth in unit sales year-over-year, the largest among all major categories.

It marks the fifth straight year of growth for a category that has consistently outperformed the industry, which saw overall revenues increase just 1.5% in 2025. It also represents a more than doubling of revenue for the pre-roll category from just five years ago ($1.68 billion in 2021).

While that growth is slower than it has been for the past several years, it indicates maturing markets, as well as a lack of new markets opening in 2025. Only two states launched legal cannabis markets in 2025 (Minnesota and Delaware, neither of which is tracked by Headset), and though Ohio (tracked) completed its first full year of legal cannabis, pre-rolls were not allowed in the state until September.

But even while revenue and unit sales growth slowed in 2025, the market share for the category not only continued to grow, but accelerate. At 15.9% market share, pre-rolls remained the third-largest category by market share (behind flower and vape pens), but the category’s share grew 7.6% year-over-year, up from 7.5% growth the year before and its strongest year-over-year growth ever and its fifth consecutive year of growth.

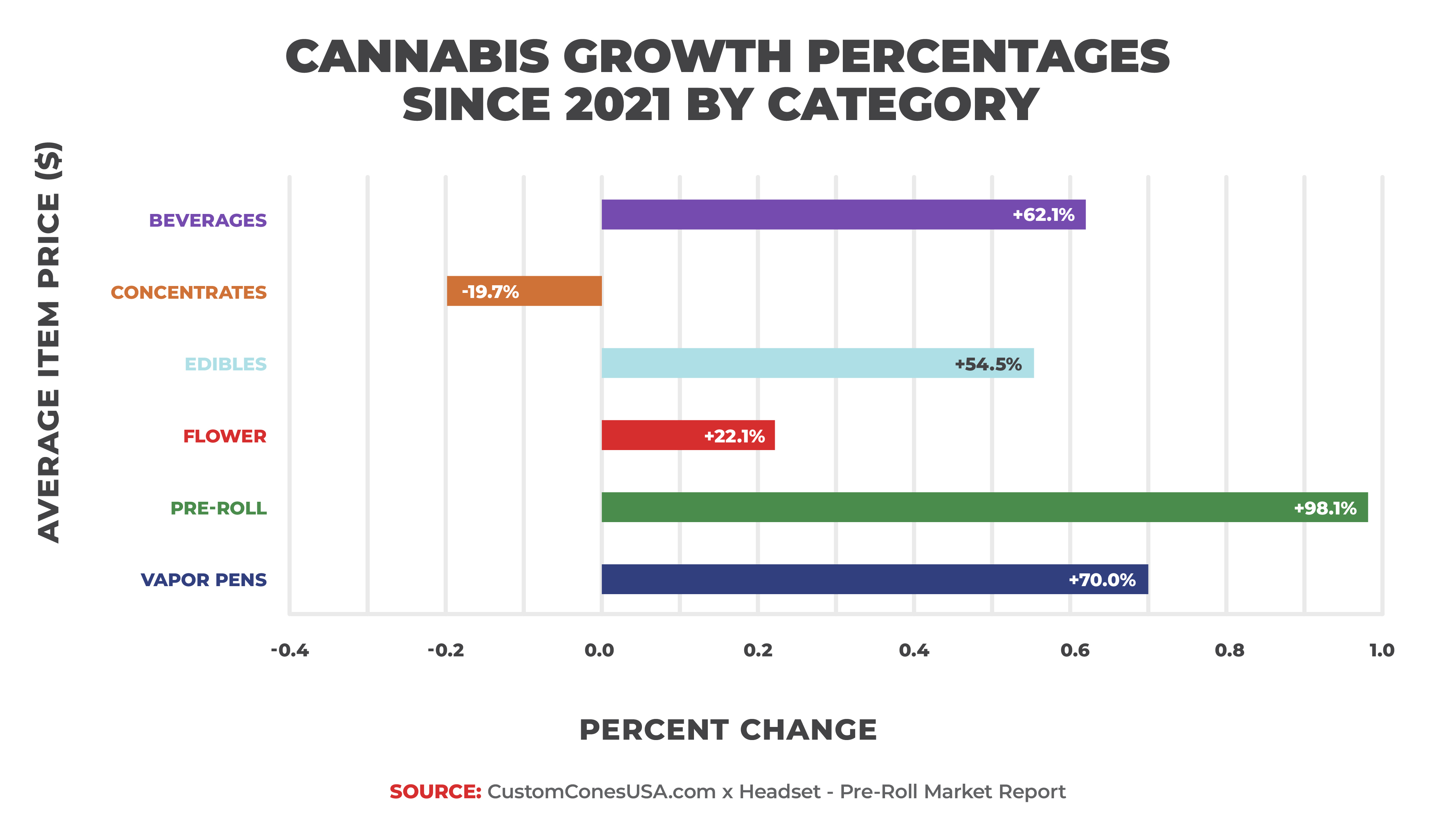

It is also the largest growth of any major category (beverages grew at a larger percentage, but the entire category is 1/10th the size of the pre-roll category) year-over-year and a massive five-year growth of 29.5%, easily the highest of any category. Over the same time period, the second-highest growth in market share was just 11%, in vapor pens, while flower fell 17.8% and concentrates fell even further at 44.2%.

In fact, in every recreational state and 14/15 total markets covered by Headset, pre rolls gained in market share, whether the overall market grew or not, indicating that while the overall cannabis market may be softening some, pre-rolls remain a favorite and overall driver of revenues and unit sales.

Pre-Roll Market Performance by State Markets

Key Stats

- California led in revenue at $703.5M, while Michigan followed ($599M) and led in volume with 133.4M units sold

- New York showed the fastest growth, up 96% in revenue and 120.4% in units year over year

- Massachusetts ranked third with $344.9M in revenue, followed by Washington at $211.3M

- Pre-roll market share increased across 14/15 tracked recreational markets, even where sales declined

Next, let’s look a little deeper into the individual markets to see where pre-rolls are the most popular.

Unsurprisingly, California tops the list of pre-roll revenue. With a huge customer base to draw from and a cultural history of cannabis, the California market is the largest in the nation and that is true for the pre-roll category as well. California pre-rolls generated $703.5 million in 2025 on sales of 52.6 million units, both down slightly from 2024.

However, the state that buys the most pre-rolls is by far Michigan, more than double the number bought in California. According to the data, Michigan residents bought a whopping 133.4 million pre-rolls in 2025, generating $599 million in revenue. That’s even more impressive when you consider that California has a population of about 4 times that of Michigan.

The primary differences between the two states are price point and the product segment that leads the way, but we’ll get to that in a minute.

Massachusetts ranks third in both categories with $344.9 million in revenue on 37.9 million units sold. New York ($330.6 million on 15.9 million units) and Washington ($211.3 million on 32.5 million units) round out the Top 5 Pre-Roll States (by revenue).

And though fourth on this list, New York showed the largest year-over-year growth of any state, an explosive 96% increase in revenue and a 120.4% increase in units sold from 2024. New Jersey followed in both categories, growing 50.5% in revenue and 79.2% in units sold. Interesting to note, Connecticut ranked third in unit sales growth at 41.4% showing that the Tri-State Area is moving toward pre-rolls in a major way.

2025 Pre-Roll Sales by State

Missouri ranked third in revenue growth with 26.3% and fourth in unit sales growth, indicating another market on the rise.

There are a handful of markets that appear to have plateaued, however. California, for example, while still No. 1 in revenue saw a drop of 3.3% year-over-year and a 0.1% drop in unit sales.

Washington, though still in the Top 5 of revenue, saw its total drop 2% year-over-year in revenue and 2.2% in units sold.

Nevada also saw revenue fall 7.2% and units sold fall 9.5%, but the product’s market share still grew in 2025, indicating a softening of the overall cannabis market, not just the pre-roll sector, which may be related to a drop in tourism experienced in the Silver State.

In fact, in every recreational market tracked, the pre-roll category grew in market share, whether the category revenue or unit sales numbers were up or down, indicating that pre-rolls are growing as percentage of the marketplace even as the overall cannabis industry is softening a little.

Massachusetts has the highest market share for pre-rolls at 20.9%, followed by New York (20.9%) and Michigan (19.4%).

Segments Within the Pre-Roll Category

While the pre-roll category as a whole continues to drive growth for the whole industry, not all pre-rolls are created equally. When we look deeper into the segment numbers, a few trends that are propelling the category jump out.

Infused/Connoisseur Pre-Rolls Dominate

Key Stats

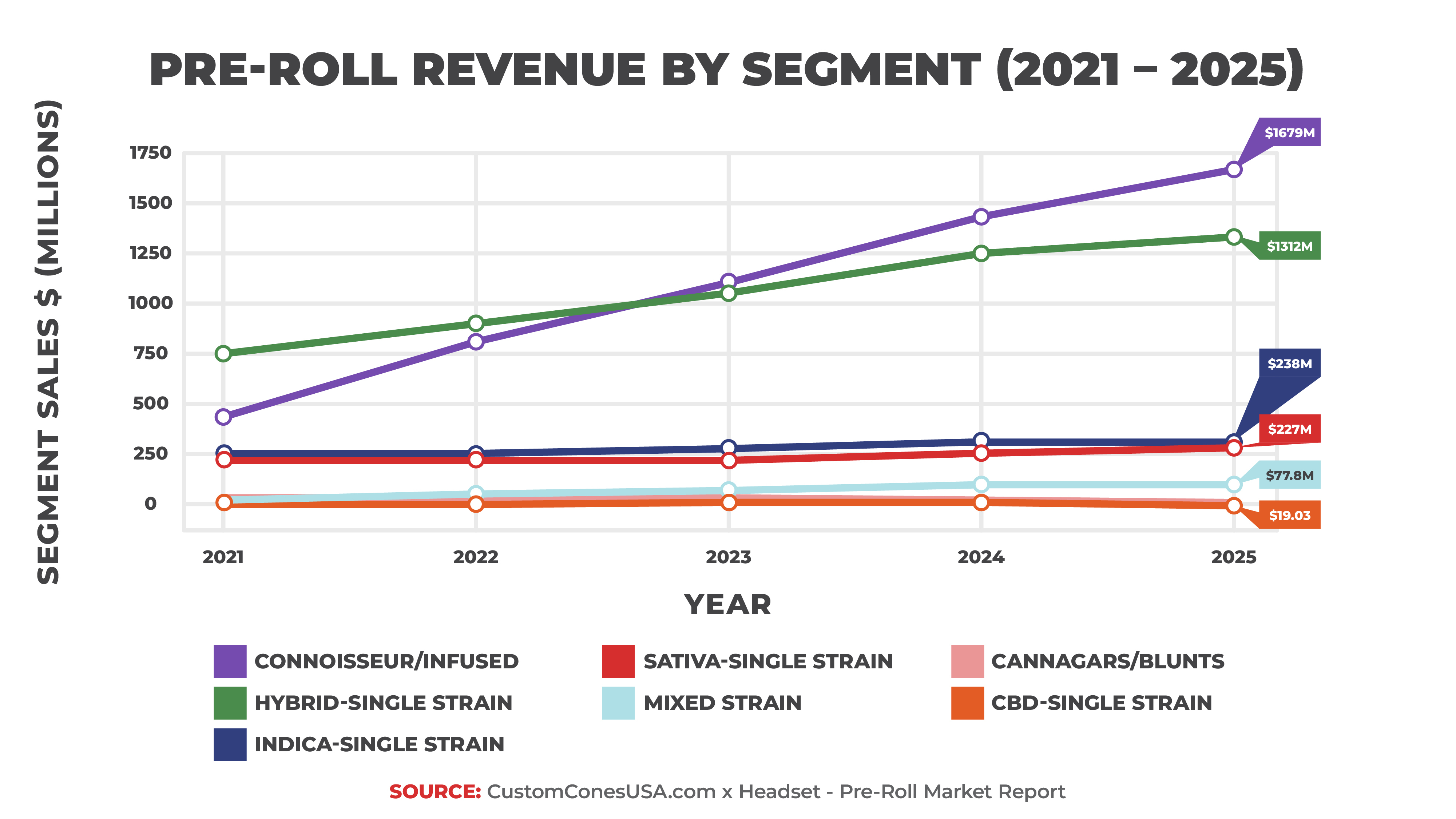

- Infused pre-rolls: $1.68B in revenue, 47% share, with +27.8% unit growth

- Hybrid pre-rolls: 175.6M units and $1.3B in revenue, leading in total volume

- Infused and Hybrid products: accounts for 84%+ of total category sales

Two years ago, the infused pre-roll took over the top revenue segment of the category and has never looked back, continuing to grow.

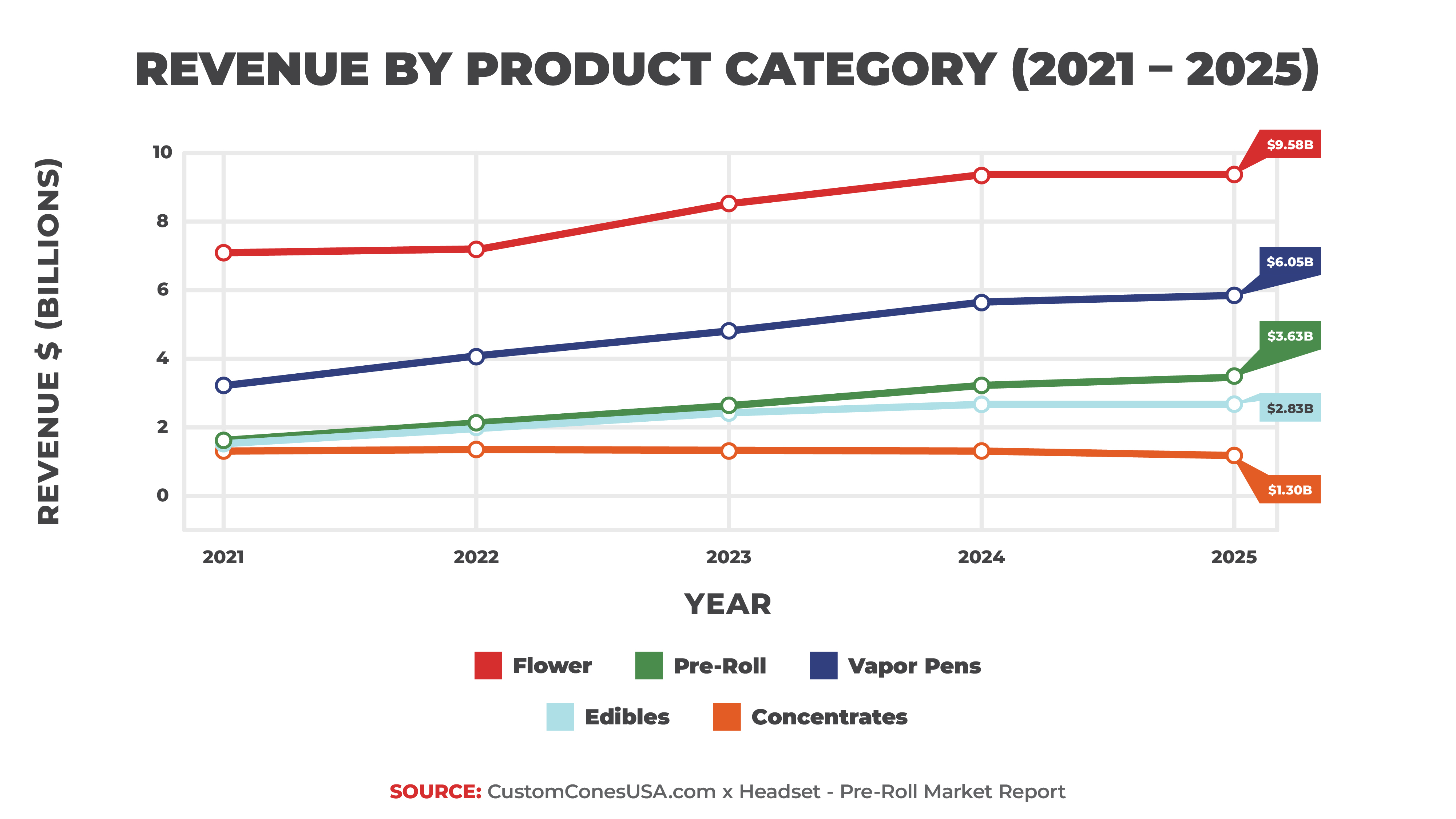

In 2025, the infused segment, which combines flower and a concentrate to create a more potent and flavorful pre-roll, accounted for $1.68 billion in revenue, or about 47% of all revenue in the category. That’s up from $1.44 billion in 2024 when it accounted for just over 44%.

The Infused pre-roll revenue is driven in part by a higher price point for the products and has been buoyed in recent years by advances in automation that allows businesses to scale up their infused production while keeping costs under control.

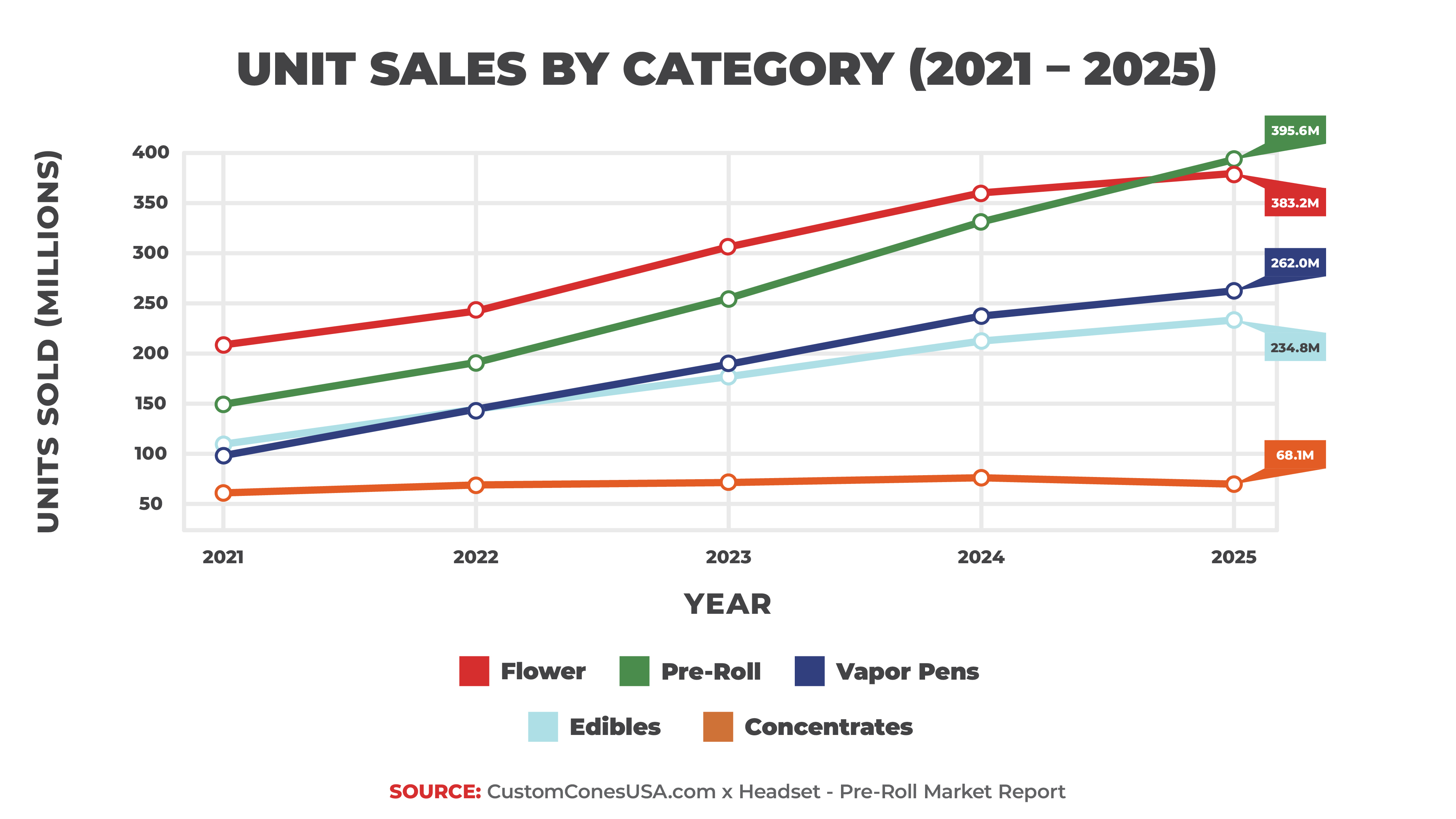

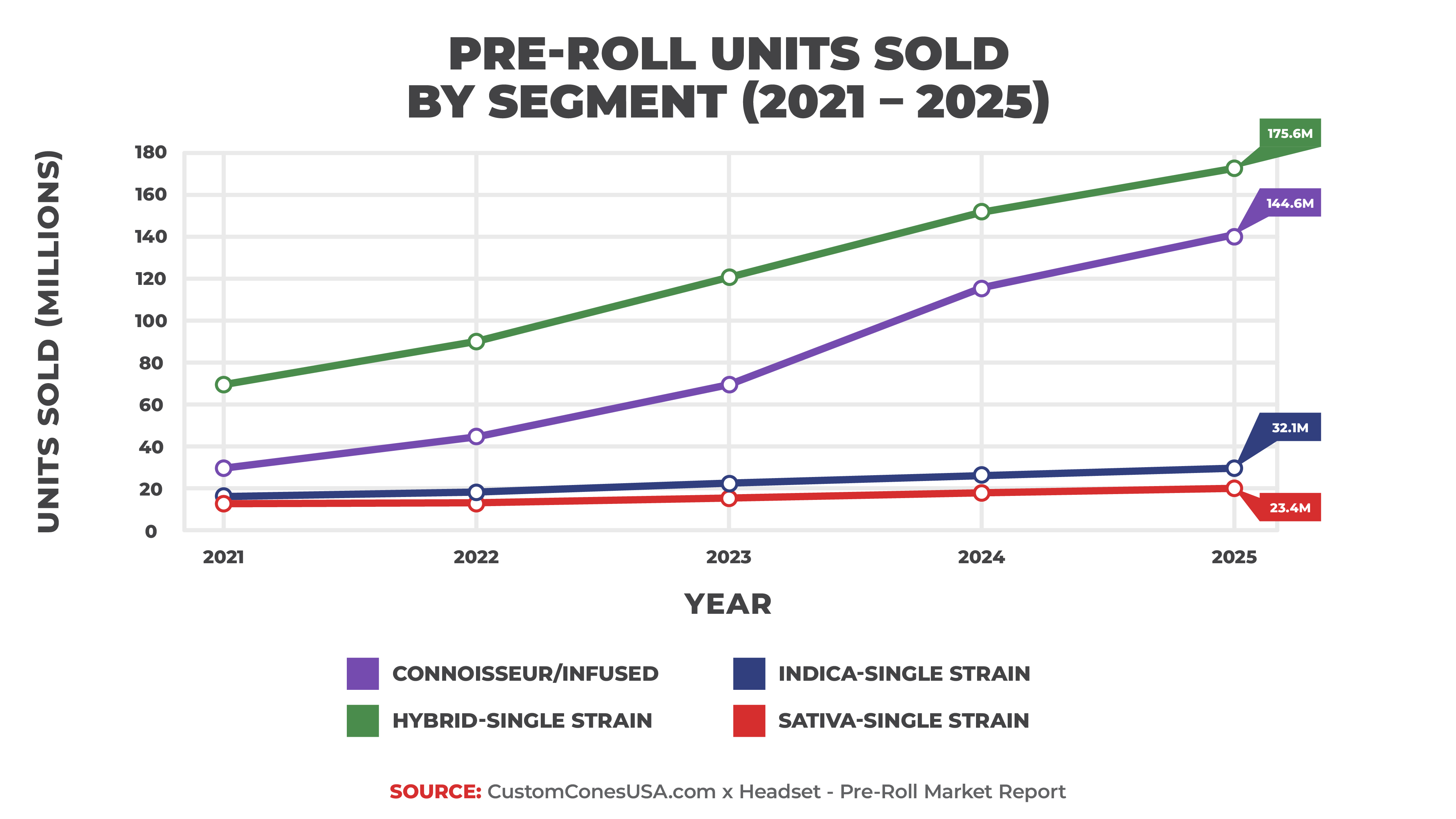

When we turn to the unit sales numbers, the Hybrid – Single Strain segment moves to the top spot, selling 175.6 million units, compared to 144.6 million for infused pre-rolls. It is the fifth consecutive year that the Hybrid – Single Strain segment has led in unit sales.

However, because of a lower price point, its revenue tops out at 1.3 billion, more than $300 million less than infused pre-roll products.

It should also be noted that infused products saw the biggest growth in both unit sales (27.8%) and revenue (16.4%) as more people reach for these innovative and potent products.

Together, the Infused and Hybrid segments account for more than 84% of all pre-roll revenues and nearly 84% of all units sold.

Rounding out the category, Indica – Single Strain brought in $238.1 million, Sativa – Single Strain took in $277.4 million and Mixed Strain followed at $77.8 million with Cannagar/Blunts at $16.3 million and CBD at $5.87 million, though the Blunts numbers are a little deceptive and we will get to that later.

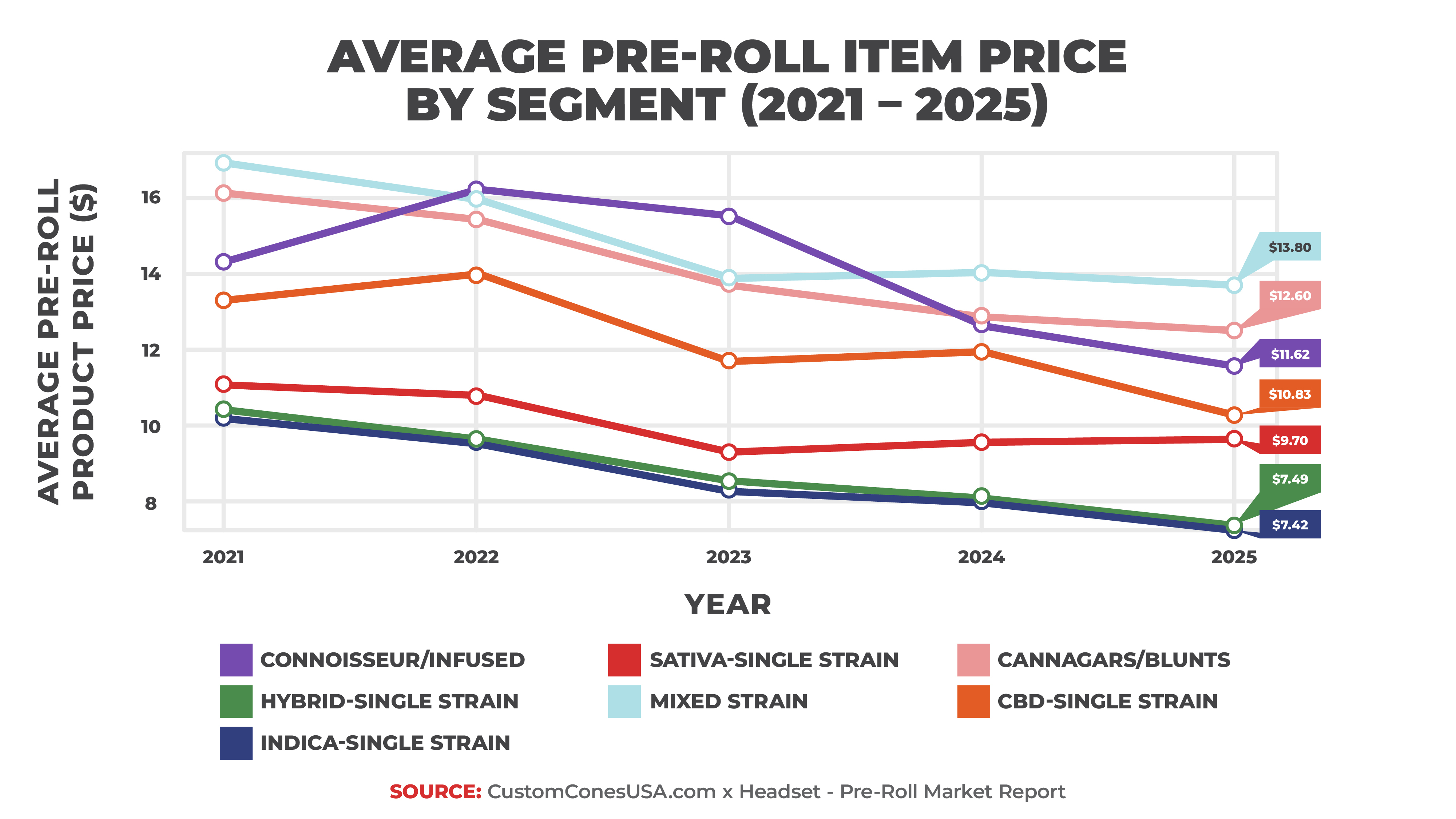

Pre-Roll Pricing in 2025

Key Stats

- Average pre-roll price fell to $9.31 in 2025, down 6.6% YoY and nearly 20% from the 2022 peak of $11.70

- Mixed Strain led in average item price at $13.84, but pricing is skewed by large multi-pack formats

- On a 1-gram basis, Infused is the most expensive segment at $7.50 per gram versus $4.50 for Mixed Strain

- Equalized average price reached $5.95, with average retailer cost at $3.23

One of the reasons for the continuing rise of the pre-roll category is a relatively low price point that allows for experimentation and encourages trying new products, however, the average price of a pre-roll product varies greatly depending on the segment and the state in which it is sold.

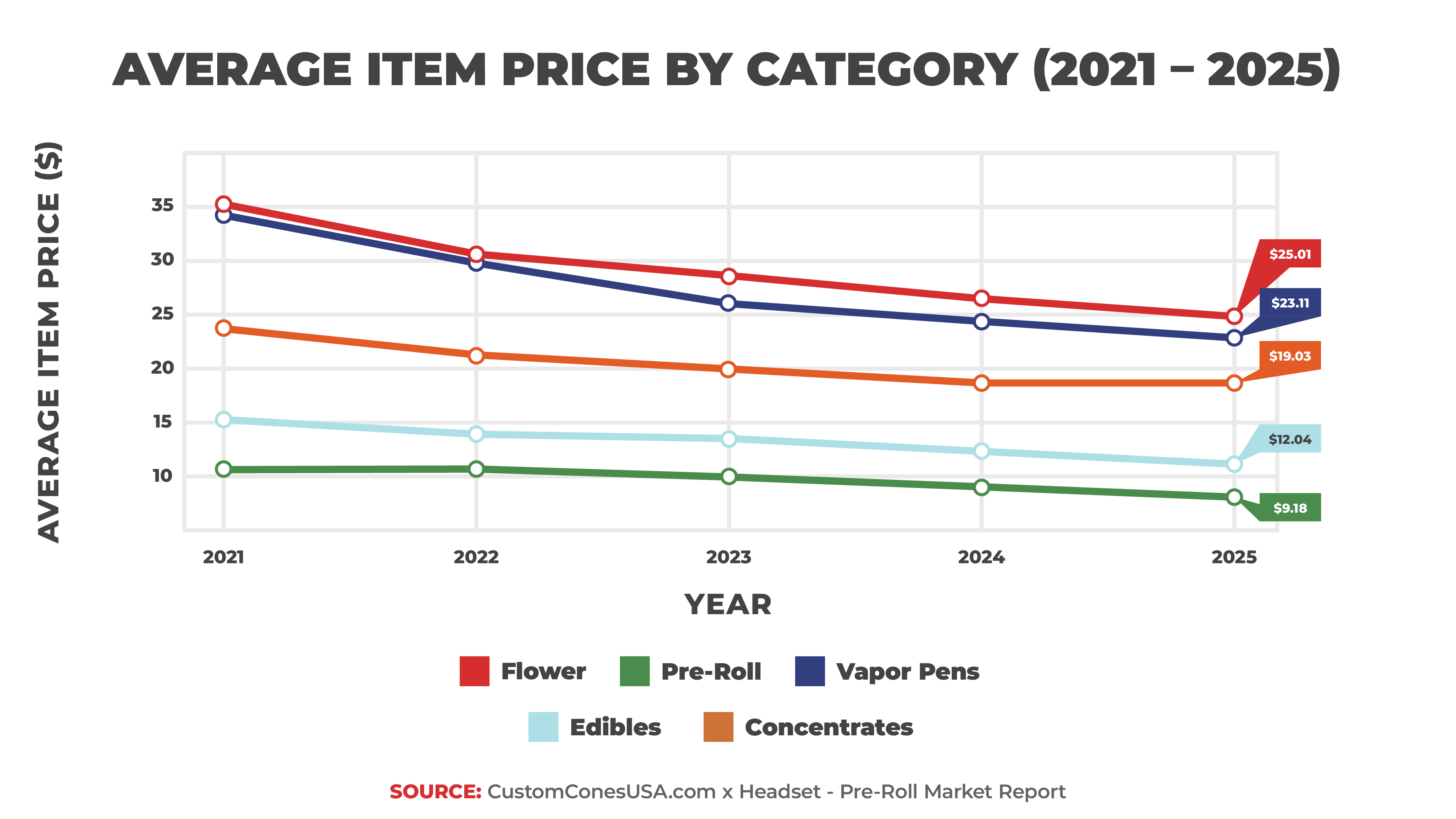

Overall, the average price of a pre-roll continues to decline as the market matures and flower becomes more available for pre-rolls. In 2025, the average price dropped to $9.31, down 6.6% from 2024’s average of $9.97 and down nearly 20% from the 2022 peak of $11.70.

Within the segments, mixed strain pre-rolls have the highest average price at $13.84. Infused products have an average price point of $11.64.

However, because of packaging sizes, those numbers do not tell the whole story. For example, mixed strain pre-rolls have the highest average price, but mixed strain products have an outsized reliance on large multi-pack formats, while infused products are more concentrated at the 1-gram size.

For example, a 28-gram mixed strain product, which accounts for 5.6% of all mixed-strain products sold, counts as a single unit, inflating the average price. Infused pre-rolls, on the other hand, barely sell any 28-gram products (literally only 31 during the whole year).

When equalized for a one-gram product, the list practically flips, with infused pre-rolls coming in the most expensive at a per-gram price of $7.50 compared to the Mixed Strain equalized price of $4.50 per gram, sixth place in the seven-segment category.

Overall in 2025, the average equalized price of a pre-roll in 2025 was $5.95, with the average cost to retailers equalized at $3.23.

Profit Margin: House Brands Vs. Non-House Brands

Key Stats

- House brands averaged $5.33 per unit with a 55% margin, compared to $9.64 and 46.2% for non-house brands

- Lower costs for house brands at $2.40 per unit versus $5.19 for non-house brands drive margin advantage

- Pre-rolls averaged a 46.6% margin overall, ranking third among major cannabis categories

Though not allowed in every state, vertical integration – in which companies are allowed to own licenses in both manufacturing and retail cannabis operations – can create unique pricing and profitability strategies through the use of “house brands,” or products that a manufacturing company sells in its own dispensaries.

For example, in the pre-roll category, house brand items account for 4.3% of revenues.

Packing the pre-rolls within the same corporate structure eliminates a middle man, lowering price points all around.

House brands price their pre-rolls lower, averaging $5.33 per item in 2025 (down from $6.75 in our 2024 report) versus $9.64 (down from $9.83) for non-house brands.

But because house brand pre-rolls are made, essentially, in-house, they eliminate a middleman and the cost to the dispensary drops, creating a larger profit margin for house brands compared to non-house brands.

According to the data, house brands have an average cost of $2.40, which creates a profit margin of 55%, compared to the non-house brand cost of $5.19 and profit margin of 46.2%.

Overall, pre-rolls have a profit margin of 46.6% on average, third among the major categories. Edibles lead the way at 47.9%, followed by vapor pens at 46.7%, pre-rolls at 46.6%, flower at 46.4% and concentrates at 43.1%.

Pre-Roll Brand Performance in 2025

Key Stats

- Jeeter ($253M) and STIIIZY ($121M) lead in revenue

- Dragonfly leads in volume with 22.6M units and $30.7M in revenue

- Premium pricing reaches more than $38 per unit, while value products go as low as $1.34 per unit

In all, the number of brands offering pre-roll products in 2025 held steady from the year before, increasing by only 72 brands to 3,242.

That is the smallest growth in brands offering pre-rolls over the past five years, which points to a maturing market and increased competition.

But while the top-level numbers held steady, a deeper look reveals some of the churn in the industry from the prior year. In total, 589 brands that were active in 2024 were not active in 2025, though 661 new brands appeared to take their place.

Within the brands themselves, the hands-down leader in revenue is California-based Jeeter. Known primarily for its infused offerings, Jeeter generated $253.2 million in revenue in 2025, selling 11 million units. STIIIZY placed second with $121.2 million in revenue, followed by Dogwalkers at $80.8 million, Cali-Blaze at $74.9 million and RYTHM at $50.8 million.

House Brand pre-rolls, those made by the dispensary in states that allow it, also sold $151.6 million worth of pre-rolls.

However, when we look at the top charts by units sold, Dragonfly Cannabis of Michigan – which does not crack the Top 10 in revenue – soars to the top, selling 22.6 million pre-rolls, more than twice second-place Jeeter’s 11 million. Cali-Blaze ranks third at 10.9 million units, followed by Goodlyfe Farms at 10.5 million and STIIIZY at 6.3 million.

House Branded pre-rolls moved an additional 28.6 million units.

Top Pre-Roll Brands of 2025

Cast Study: Jeeter vs. Dragonfly

Key Stats

- Jeeter leads in revenue with $253M, driven by premium infused multi-pack products

- Dragonfly leads in volume with 22.6M units sold, built on a low-price, high-volume model

- Jeeter averages $23.06 per unit versus $1.34 for Dragonfly, highlighting a wide pricing strategy gap

- The category supports both premium multi-pack strategies and value-driven single-unit models

There are two undisputed kings of the pre-roll category, depending on which metric you choose to focus on.

Jeeter, the California-based brand that specializes in high-end infused prerolls rakes in more than twice the revenue of its closest competitor, dominating sales charts to the tune of more than $253 million in 2025. In total, the company sells pre-rolls in six states: California, Michigan, Massachusetts, New York, Arizona and Missouri.

Michigan-based Dragonfly Cannabis, on the other hand, sells more than twice as many pre-rolls as its nearest competitor, climbing to the top of the unit sales charts with 22.6 million units sold, but does not even rank in the top 10 in revenue, collecting just $30.7 million. They operate in Michigan and New York.

The difference is the product and price point offered by each leader, offering different strategies and roadmaps to success for pre-roll brands.

Jeeter sells premium, infused pre-rolls with an average price point of $23.06 per unit. Dragonfly, on the other hand, focuses on selling primarily single-strain traditional pre-rolls with an average price point of $1.34, the lowest average price for all pre-roll brands.

Dragonfly also predominantly sells 1-gram individual pre-rolls, aiming for high-volume sales, while Jeeter’s most popular products are 2.5-gram 5-preroll multi-packs, which also helps drive up its average price.

Other brands that focus on premium pricing models are Ruby Farms ($38.35/unit), Lowell Herb. Co. ($34/unit), RYTHM ($28.25/unit) and Rove ($27.91/unit).

Other brands that aim for volume sales include Goodlyfe Farms at $2.83 per unit.

Mid-Tier Brands that split the difference include Cali-Blaze ($6.83/unit) and Presidential ($16.53/unit).

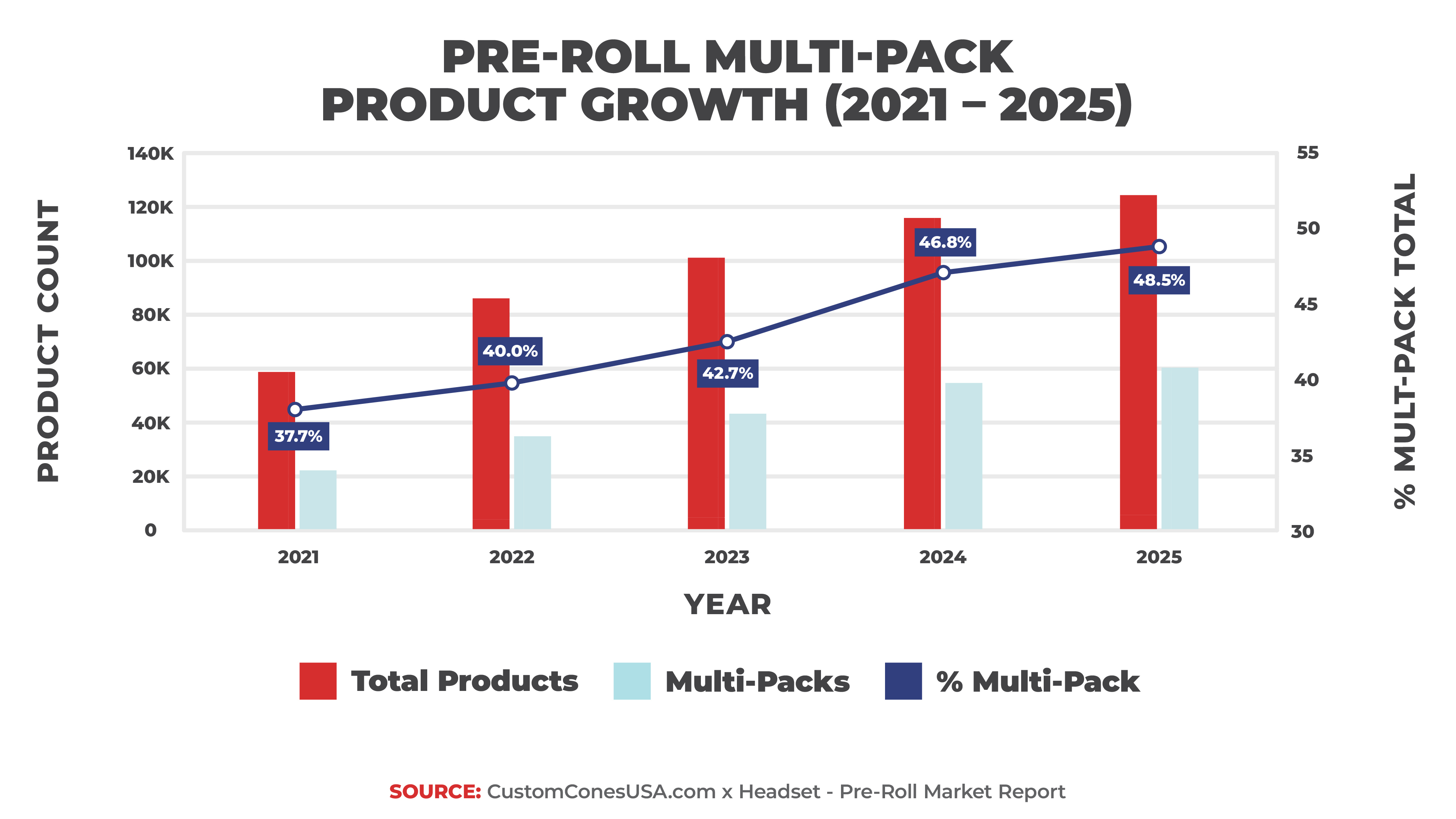

Ascendance of the Pre-Roll Multi-Pack

Key Stats

- Multi-packs account for 48.5% of SKUs, up from 37.7% in 2021

- 90% of top 100 products are multi-packs

- 2.5g 5-pack leads with $612M in revenue and 17.2% share

- 1g single remains the top individual format with $1.44B in revenue

Over the past several years, we have seen the ascendance of multi-pack formats as consumers' preferences shift toward larger package sizes. But in 2025, the multi-pack truly dominated the sales charts with its largest growth in five years.

In 2025, a full 48.5% of pre-roll products were multipacks, up from 46.8% the year before and from 37.7% in 2021. Even more telling, however, is the multi-pack's dominance on the sales charts, with 90% of the Top 100 products coming in the multi-pack format. That’s up from 78% in 2024 and the largest jump in five years.

The 2.5-gram 5-pack format is by far the most popular multi-pack, generating $612 million, or about 17.2% of total pre-roll revenue and nearly 24 million units sold. According to Headset, there are 9,817 distinct 2.5-gram format products.

The multi-pack is becoming a consumer favorite for a handful of reasons, mainly a lower price-per-unit cost and the convenience of being able to stock up and visit the dispensary less frequently.

For manufacturers, multi-packs can bring higher revenues with better margins (due in part to lower packaging expenses) and help lead to brand loyalty through larger purchase commitments that keep customers coming back.

In our survey results, 72.4% of manufacturers said they sell their pre-rolls in multipacks, with 5-packs being by far the most popular (50% of multi-pack sellers). The 2-pack is also popular, with 26.1% of multi-pack sellers offering 2-packs. As for larger packs, 21.7% sell 8-10 pre-roll packs while only 18.5% sell multi-packs with 14 or more pre-rolls per pack.

Additionally, we found that single-strain multi-packs are the most popular, with 54.4% of manufacturers making those compared to just 9.8% selling variety packs, though 35.9% sell both.

That said, it should be noted that the 1-gram single is the top-selling single-size product, generating $1.44 billion in 2025. So while multi-packs are important and growing in popularity, the standard 1-gram pre-roll is still a must-have in every product lineup.

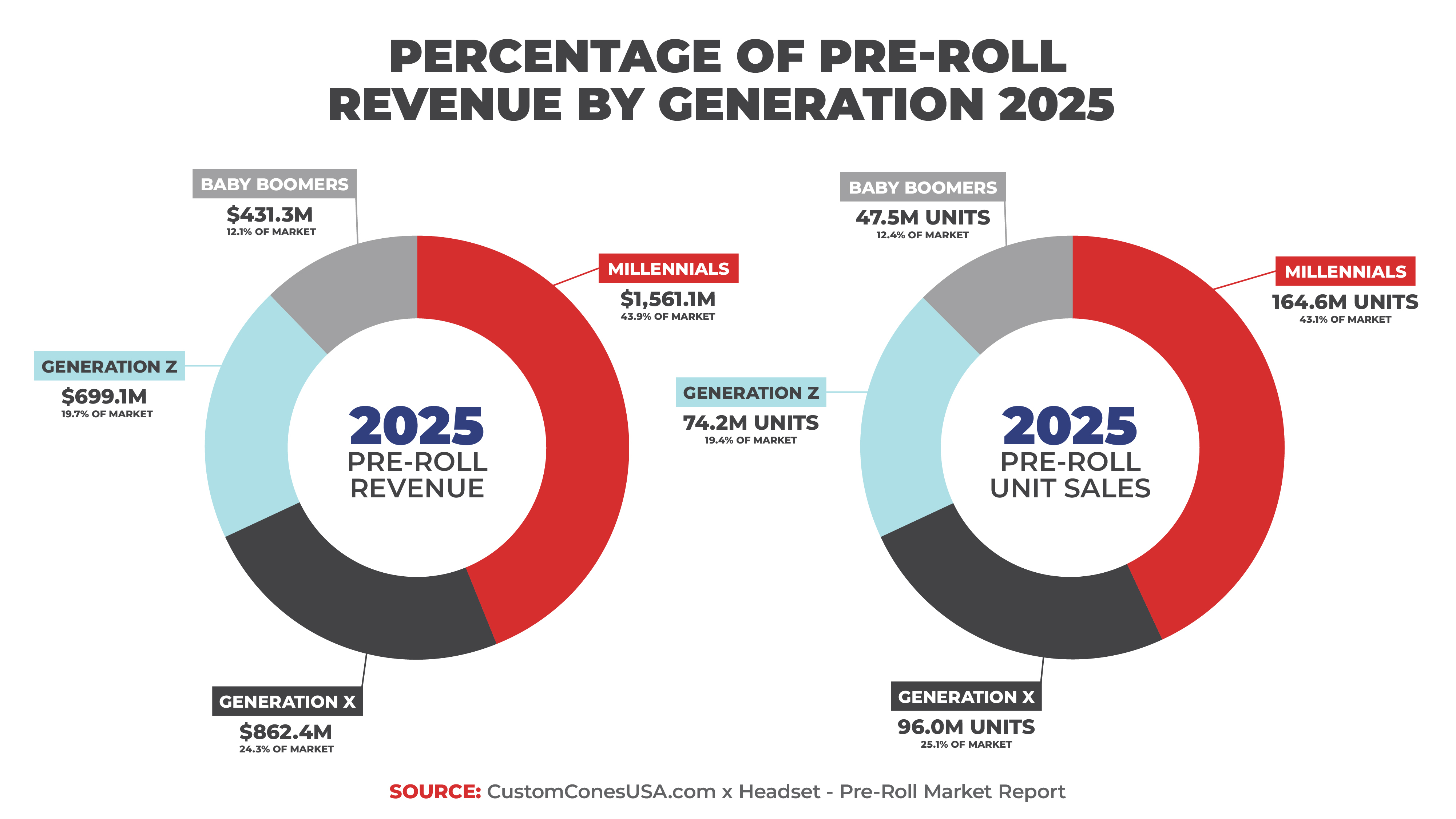

Who is Buying Pre-Rolls Today

Key Stats

- Millennials account for 43.9% of revenue, totaling $1.6B

- Category skews nearly 60% male, with Millennial women as the second-largest segment

When it comes to buying pre-rolls, one generation easily takes the top spot. No group buys more pre-rolls than Millennials, and it’s not even close.

Millennials account for a full 43.9% of pre-roll revenues and 43.1% of units sold, accounting for $1.6 billion in sales in 2025 on 164.6 million units sold.

And though males account for 58.9% of all pre-rolls purchased and 60.2% of the pre-roll money spent, Millennial women buck the trend again, soaring to the no. 2 spot on their own, just behind Millennial males and ahead of Generation X men and Gen Z males.

Generational buying habits largely mirror 2024 numbers, though there have been some shifts with Gen Z showing the largest growth in terms of revenue (16.8%) and second in units sold (22.1%).

And as in prior years, Baby Boomers remain the smallest generational market share at 12.1% of revenue and 12.4% of units sold. However, Boomers as a group saw the strongest growth in units sold with a 23.5%.

And, important to note, pre-rolls saw growth in revenue and sales across every demographic in 2025, once again showing the wide appeal and resilience of the product category.

New Pre-Roll Products

Key Stats

- 63,552 new pre-roll products launched in 2025, with more than 50% as multi-packs

- Hybrid - Single Strain led with 28,941 new products, followed by 22,381 Infused products

- Hybrid and Infused segments accounted for 81% of all new product launches

In total, 63,552 new pre-roll products were released in 2025, down from 66,056 in 2024. However, for the first time ever, more than 50% of all new products offered are multi-packs.

Of those new products, 28,941 were Hybrid – Single Strain products, the most new products in any single segment, with 51% being packaged as multi-packs.

Another 22,381 were Infused pre-roll products, with 45% of those being multi-pack offerings.

Combined, those two segments account for 81% of all new pre-roll products introduced in 2025.

Pre-Roll Opportunities

Key Stats

- Premium tips represent just 0.03% of total sales

- Blunts, the 3rd most popular consumption method, controls only 4.2% of total sales

After analyzing the data, we have identified two areas of opportunity for pre-roll manufacturers: premium filter tips and pre-rolled blunts. Both categories are underrepresented in the data and provide places where smart brands can establish a leg up in a very competitive marketplace.

Premium Glass, Wood, & Ceramic Filter Tips

It’s difficult to get a true read on exactly how big the premium filter tip segment is because it is not specifically broken out in the data. But an exploration of the Headset product database reveals a very small number of products that contain names that include a premium filter tip option, which we define as a wood, glass or ceramic filter tip.

Only 205 SKUs clearly offer premium filter tip options, with glass being the most common. In total, these account for just 0.03% of pre-roll sales.

However, as part of our consumer survey, more than 21% of respondents told us they purchase pre-rolls with premium filter tips at least once weekly, indicating openness to enhanced smoking experiences.

Though currently a niche product, we see this as a huge potential growth market and an opportunity for brands to make a mark on the industry with memorable, premium pre-roll products.

The Blunt Opportunity

According to Headset, pre-rolled blunts currently make up less than 1% of total pre-roll sales. Of the $3.6 billion generated by pre-rolls in 2025, the “Cannagar/Blunt” segment accounted for roughly $16.3 million in sales, or so it seems.

However, because of how Headset parses the data, infused blunts fall into the “connoisseur/infused” segment, not the blunt segment, skewing the final numbers.

When we look specifically at the products containing the word “blunt,” we get a clearer picture. Collectively, those “blunt” products sold 8.5 million units and generated more than $148 million in revenue nationwide, accounting for 4.2% of total pre-roll sales.

On top of that, New Frontier Data released a study that found blunts are the third-favorite method of ingestion, leading us to believe there is an entire market of blunt smokers ready to buy the right pre-roll blunt products.

That demonstrates a demand for the product. And for pre-roll producers and processors, that’s the definition of a growth opportunity.

Checking our survey results, only 36.2% of our respondents make a blunt product, though an additional 15.8% are planning to launch one.

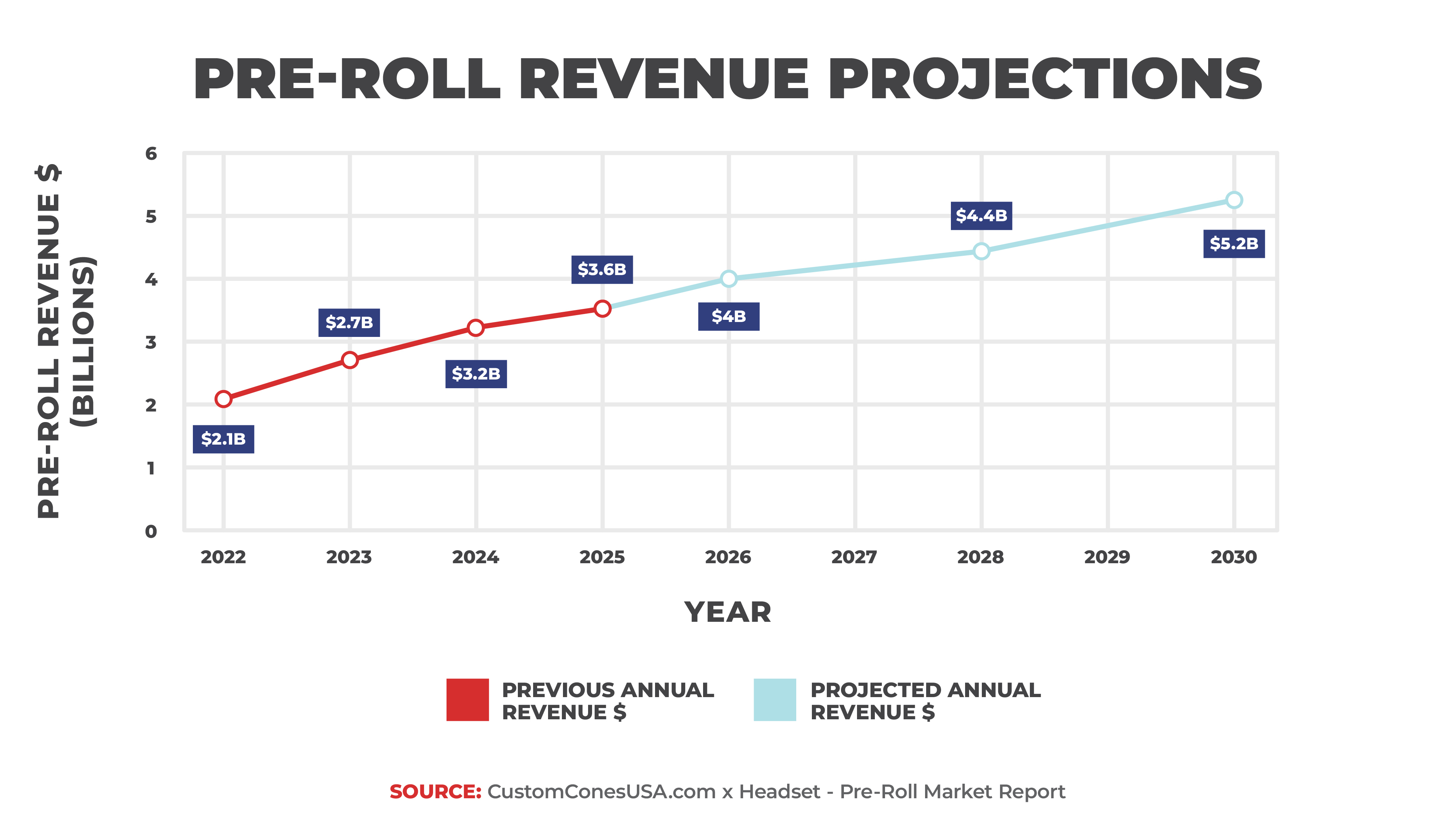

Pre-Roll Market Predictions

Key Stats

- Projected 2026 growth of 5–10%, reaching $3.8B to $4B

- Infused segment expected to grow 15%

- Mid-Atlantic markets, including New York, New Jersey and Connecticut, are key expansion regions

- Long-term growth projected at around 6% CAGR, reaching $5.2B+ by 2030

- Multi-packs expected to reach 60% share and dominate top-selling SKUs

While the pre-roll category continues to grow faster than the larger industry, there are signs that the cannabis market is softening and beginning to plateau. Looking forward, however, we still see the pre-roll sector maintaining its role as the primary driver for the industry as a whole.

Looking ahead to 2026, we see the pre-roll category continuing to grow at a rate faster than the industry as a whole, though not necessarily as fast as in previous years.

Given the slowdown we saw in 2025 and the lack of new state markets opening in 2026, we are conservatively predicting a growth of 5-10% for the pre-roll category, generating revenues of between $3.8-4 billion for calendar year 2026.

We also expect infused pre-rolls to continue to lead the way, outperforming the overall category with a growth rate closer to 15%, while single-strain segments may only grow at a single digit rate.

At the state level, we see continued growth in the Mid-Atlantic Tri-State area of New York, New Jersey and Connecticut, which collectively saw tremendous growth in the pre-roll sector in 2025. New York’s market continues to grow and mature, and we believe it has not yet reached its ceiling. New Jersey, meanwhile, is scheduled to open consumption lounges this year, which we believe will boost the sale of pre-rolls due to their convenience.

Similarly, Massachusetts is primed for additional growth as its Cannabis Control Commission in December 2025 also created three new consumption lounge license categories expected to go into effect this year. Massachusetts already ranks third in terms of revenue and units sold and no. 1 in pre-roll market share, but we expect to see that grow even more in the future as, again, pre-rolls are the perfect product for consumption lounges.

Expanding to a 5-year view, we see continued growth but slowing as more markets mature and price compression that increased competition brings. We conservatively estimate a compound annual growth rate (CAGR) of about 7.5%, resulting in the pre-roll market climbing to about $5.2 billion in revenue by 2030.

If new markets open or expand over that time, such as Florida, we could see larger-than-expected growth in the pre-roll market, particularly in states that have a medical infrastructure already in place.

We also predict the continued increase in multi-pack sales, which again saw its largest growth ever in 2025 to become more than 50% of all pre-roll units sold. Within 5 years, multi-packs could account for up to 60% of all products and easily take up 95 of the top 100 products.

And, again, pre-rolls are the obvious product to bet on in consumption lounges so we could see all of those numbers increase even more as more states allow for public consumption.

One of the top issues in the pre-roll sector in recent years has been the rise of hemp-derived cannabinoid pre-rolls, such as delta-8 THC, THCa and others. These products, which are available in legal and non-legal states thanks to the 2018 Farm Bill and subsequent court decisions surrounding it, are a $21.8 billion industry in 2025 and could be affecting the legal pre-roll market, contributing to the overall slowdown. However, many states with legal markets have begun to regulate these products themselves, and with no direct sales data to study it is difficult to predict what will happen in this highly volatile market.

Cannabis Rescheduling Concerns

Another variable that could affect the cannabis industry is the potential rescheduling of cannabis from a Schedule I to a Schedule III drug. In December 2025, the president signed an executive order directing the Attorney General to complete the rescheduling process “in the most expeditious manner permitted under federal law,” with completion expected this year.

While we don’t see this affecting the pre-roll segment specifically, since the product would still remain illegal except in states that have legal markets, the biggest change this could bring to the industry comes in the form of tax relief. Rescheduling should allow cannabis businesses and pre-roll manufacturers to avoid IRC Section 280E and allow them to claim Costs of Goods Sold (COGS), like any other business. This would lower the tax burden on the industry and free up additional revenue for profit or investment.

Pre-Roll Producer Survey Responses

But while the data can tell us about the pre-roll business, we can’t tell the whole story without the businesses that make the pre-rolls. That’s why we polled more than 125 representatives from companies in the pre-roll industry to better understand what pre-rolls are selling, what trends they are responding to and what challenges they are facing.

Our respondents come from all sectors of the pre-roll industry, including multi-state operators, manufacturers, dispensaries, vertically integrated companies and brands, among others. More than half – 54.2% - are producer/manufacturers with another 15.2% coming from vertically integrated companies. Just over 10% of respondents are from dispensaries only while 3% are multi-state operators.

And 88.8% of respondents work in medical or recreational cannabis, with the rest selling THCa, Delta-8, CBD or hemp pre-rolls. Operators from every medical and recreational state in the union responded, as well as from Canada.

Pre-Roll Brands Surveyed

Key Stats

- 83% of operators have teams under 25 employees

- 71.6% operate with just 1–2 pre-roll workers per production line

The pre-roll sector remains one of the most competitive in the entire industry, with only the strongest surviving for the long haul and new challengers appearing every year.

This year, 21.3% of our respondents are from new businesses, down from 39.9% in our 2024 survey. This may be related to fewer new markets opening in 2026 compared to 2024. However, as the market matures, so have pre-roll businesses and now 34% of our respondents are from companies that have made it past the 6-year mark, up slightly from our 2024 numbers.

Our poll showed that nearly 83% of the pre-roll businesses surveyed have fewer than 25 employees, though about 8% have more than 100 employees. Additionally, our results showed that the vast majority of pre-roll businesses (71.6%) typically use 1-2 employees for making pre-rolls.

This is similar to what we have seen in the past and shows that with the continuing advancements and innovations in pre-roll machines, less employee time must be spent filling pre-rolls.

Asked how they would characterize their brand, 41.7% said “premium,” 21.3% said “mid-shelf” and 23.6% said “budget friendly." Also interesting to note is that 45.5% of our respondents said they offer multiple brands of pre-rolls, presumably to capture different sectors of the customer base, including value buyer and premium pre-roll aficionados.

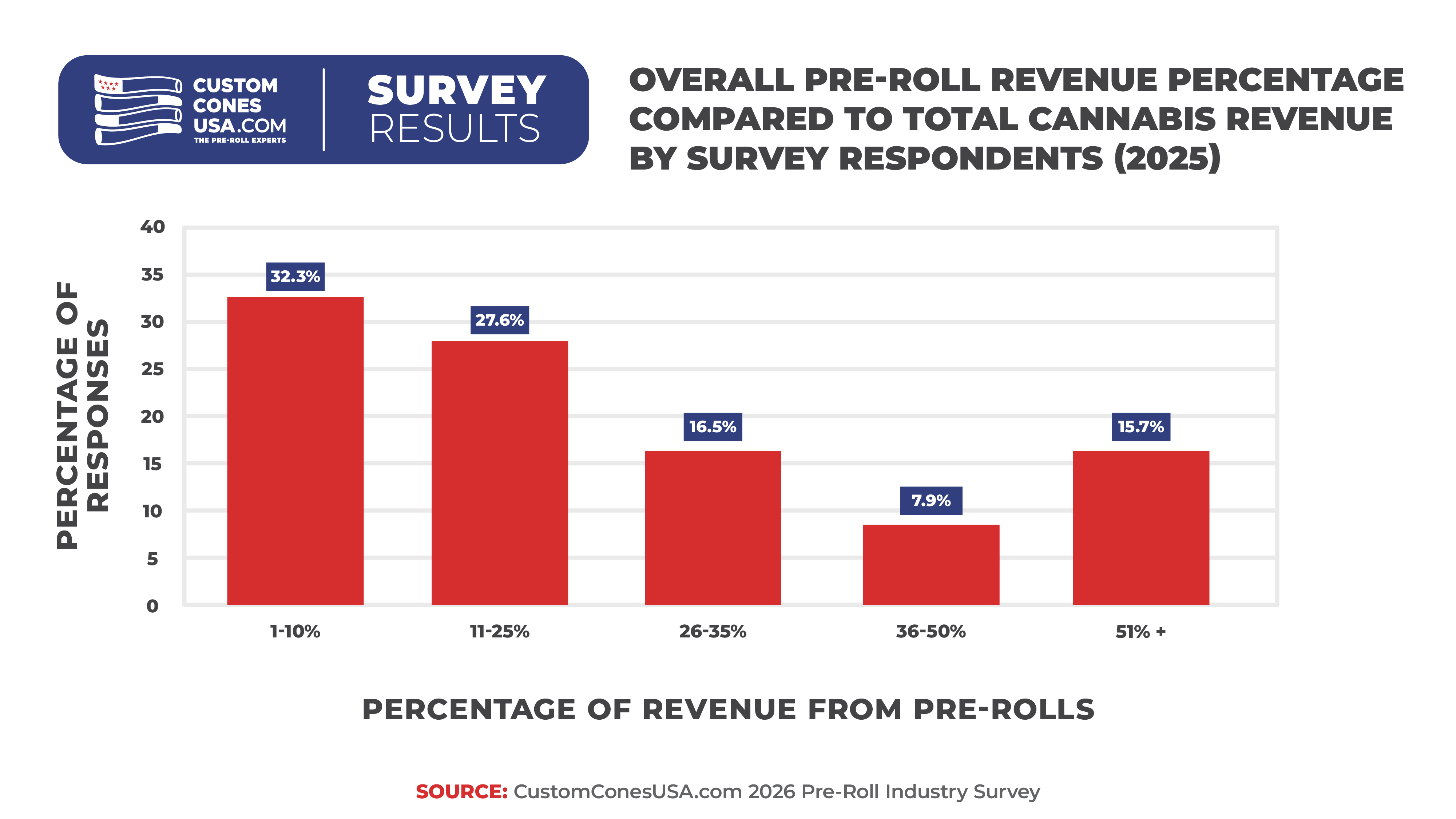

How Much of Your Business is Pre-Rolls?

Key Stats

- 59.8% of operators report pre-rolls make up 25% or less of their business

- 24.4% report pre-rolls account for 26–50% of revenue

- Pre-rolls remain a secondary but consistently growing revenue stream for most businesses

Our 2026 survey revealed that about 59.8% of respondents said pre-rolls make up a quarter of their business or less and 24.4% said that pre-rolls make up 26-50% of revenues.

Both of those numbers are down slightly and once again highlights that pre-rolls are not the main revenue source for most businesses, though they continue to provide a consistent revenue stream that makes production worth its while.

The continuous growth in the category, which outpaces the industry as a whole, as well as every other category. We also note that the largest pre-roll companies (by revenue) also offer a wide array of pre-roll products, highlighting the experimental and innovative nature of the category.

Pre-Roll Production Numbers

Advancements in pre-roll machinery, including smaller but reliable tabletop models like the King Kone and Fill N’ Fold cone-filling machines, as well as continued innovation from the companies that make those machines to include additional enhancements like closing tools or closing machinery, has helped many small- and mid-sized companies and brands enter and expand in the pre-roll space.

Additionally, advanced, automated machinery and pre-roll machines that help produce infused pre-rolls, have created a space where more companies are producing more pre-rolls than ever before.

But how many pre-rolls are being made?

How Many Pre-Rolls Can You Make?

Key Stats

- 37% of producers make fewer than 1,000 pre-rolls per month, down from prior years

- 76% now produce between 1,000 and 10,000 per month, showing production growth

- 73.2% of operators plan to expand their pre-roll product lines

With more than 66% of companies being 5 years old or less, it makes sense that 37% of our respondents produce fewer than 1,000 pre-rolls per month. However, that number is down from our 2024 survey that saw nearly 45% in that category. We see this as an indicator that pre-rolls are both easier to make and more popular today than ever before.

Nearly 20% of pre-roll businesses have mid-level production of 1,000-5,000 pre-rolls per month with another 19% producing between 5,000-10,000 per month. Both of those categories are up significantly from our previous survey results of 17.9% and 8.9%, respectively.

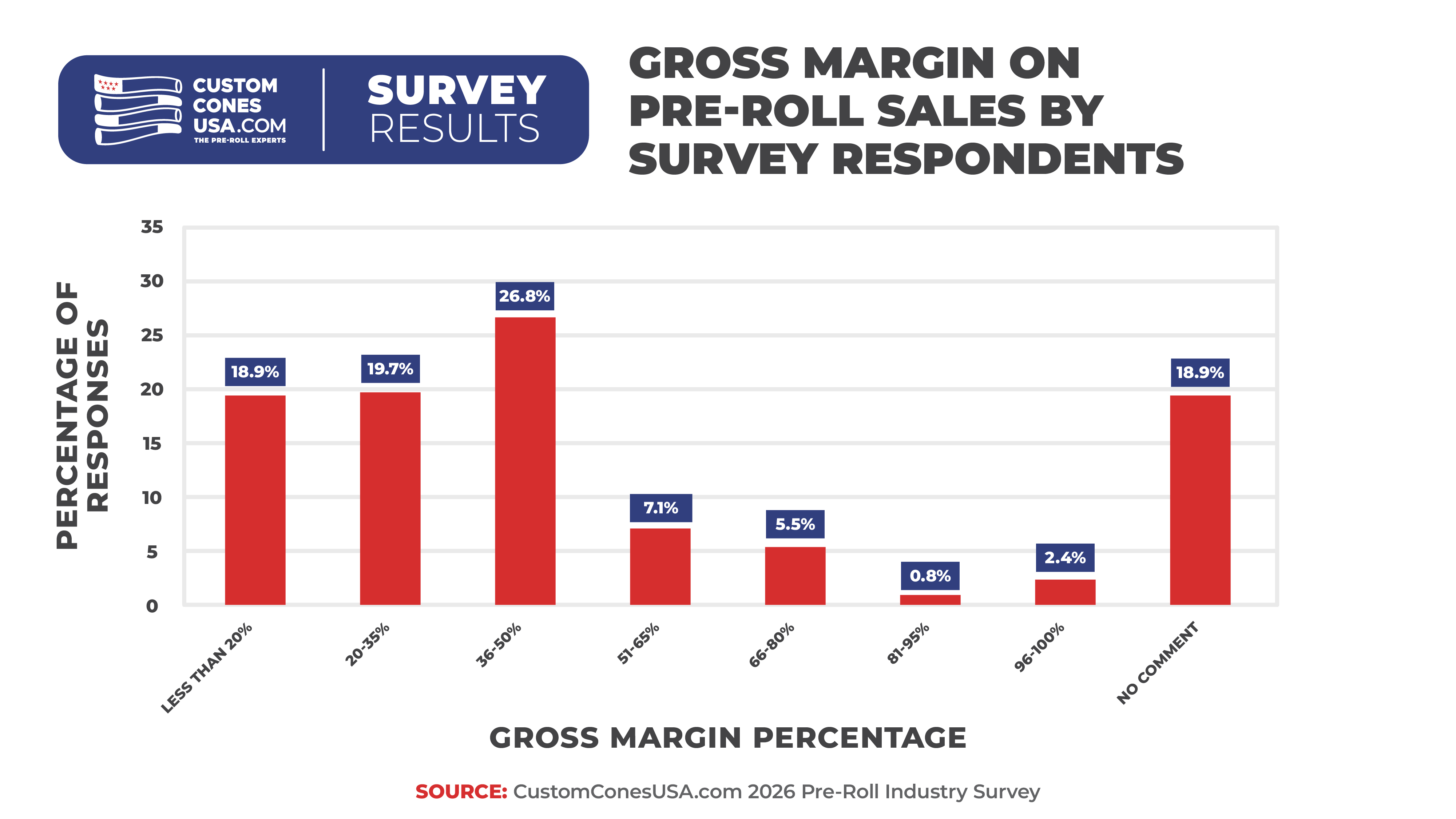

Only about 7.9% of manufacturers in our survey produce more than 100,000 pre-rolls each month.

While we do not recommend automated pre-roll machines for companies that produce fewer than 10,000 per month, mid-level pre-roll businesses could increase output and reduce costs with the addition of tabletop pre-roll machinery or closing mechanisms for the machinery they have.

However, when asked if they plan to expand their pre-roll line, 73.2% said yes, with the 35.4% saying they planned to add multi-packs and 27.6% saying plan to add a lower price point pre-roll to their line. Another 26.8% plan to add additional sizes to their line while 25.2% will be moving into the infused segment in the near future.

What Types of Pre-Rolls Are Being Made?

Key Stats

- Cones dominate production at 63%, with 1-gram pre-rolls produced by 81.9% of manufacturers

- Half-gram pre-rolls rank second at 53.5%, with sharp drop-off beyond core sizes

- Tubes account for 16.5% of production, with 20.5% of producers offering both formats

While the data gives us an idea of how many pre-rolls are selling, to get a look at what types of pre-rolls those are, we turn to our survey data to find out what the popular sizes, shapes and paper types are in the current industry.

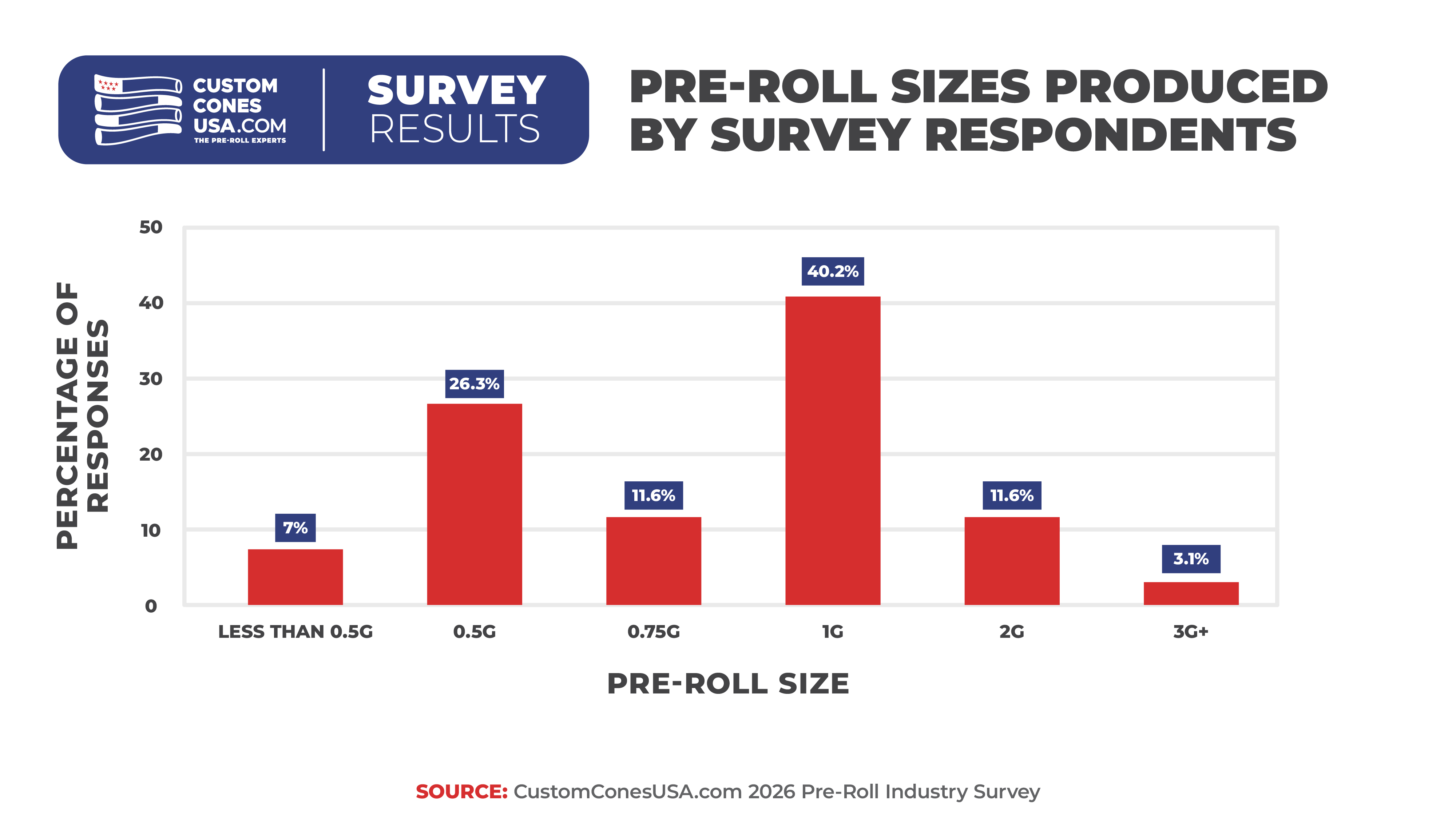

Once again, we found that the cone is the popular pre-roll shape being produced, with 63% of producers making cones compared to 16.5% packing pre-rolled tubes. Another 20.5% sell both.

As for pre-roll sizes, the one-gram – the most popular single product in the category – is unsurprisingly the top choice with 81.9% of manufacturers making a full-gram pre-roll. The second most popular size is the half gram, with 53.5% of respondents making half-gram size cones.

After the two main sizes there is a drop-off with 23.6% saying they made 0.75-gram products and the same number offering 2-gram pre-rolls. Only 15% made “mini” or dogwalker-sized pre-rolls and even fewer, 6.3% had 3-gram offerings.

What Paper & Wrap Types are Brands Using?

Key Stats

- Material usage: Refined White (49.6%), Natural Brown (48.8%), Organic Hemp (35.4%), Hemp Wrap (22.8%)

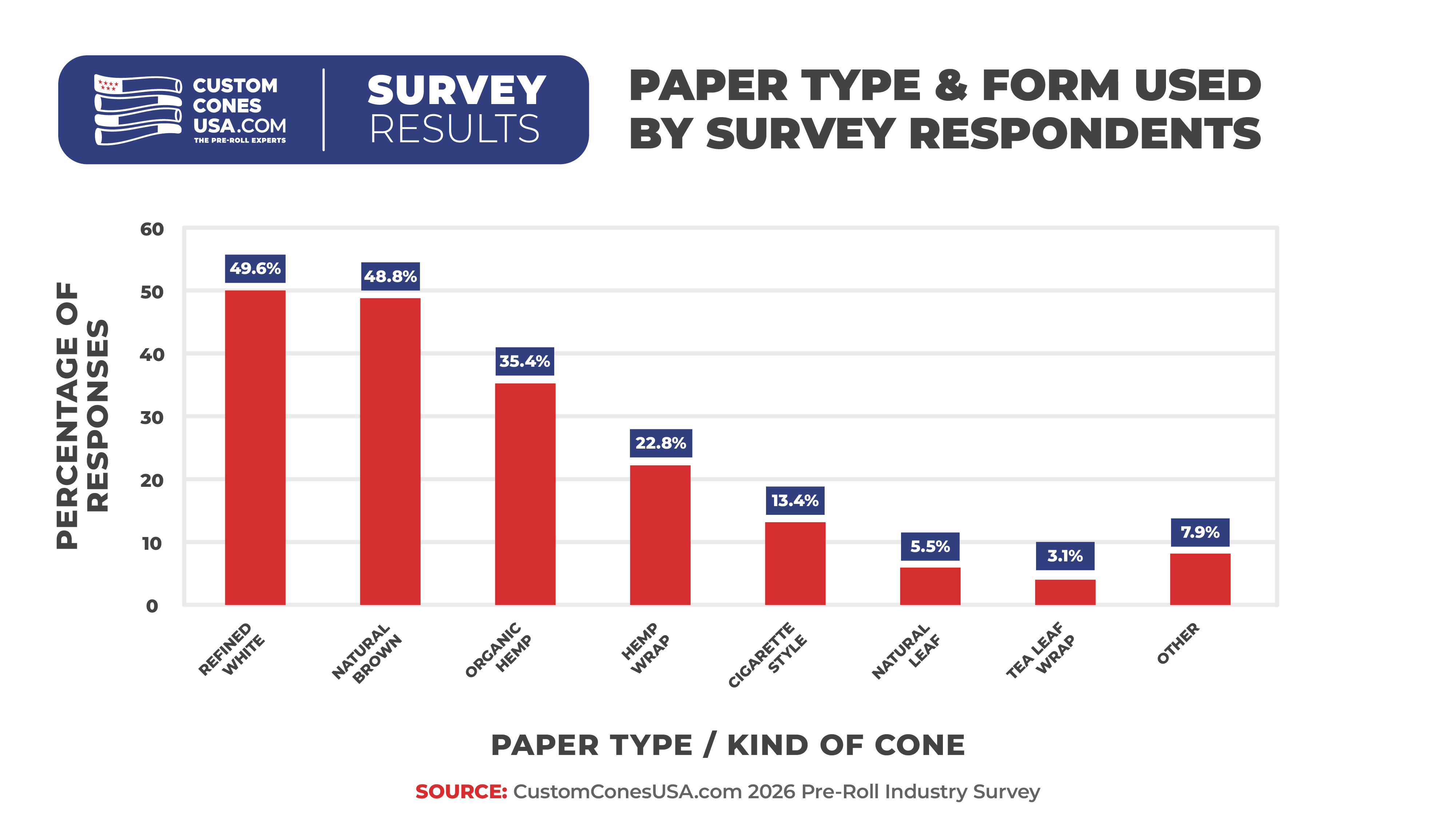

Once again, refined white paper is the most popular paper used in the pre-roll industry, with 49.6% of our respondents offering a refined white option. Natural Brown paper remains very popular, coming in second with 48.8%, followed by organic hemp paper at 35.4%.

Hemp wraps are used by 22.8% and 13.4% use cigarette-style tubes. The use of natural leaf, which can be difficult to find clean sources due to the way natural plants can absorb pesticides and heavy metals from the environment, dropped to 5.5% this year.

As for closing method, the Dutch crown-style fold is the most popular, with 55.1% closing their pre-rolls that way compared to 35.4% for the twist. Another 3.2% use silicone caps to top their pre-rolls, avoiding closing altogether.

Do You Sell Infused Pre-Rolls?

Key Stats

- 65.4% of producers sell infused pre-rolls, with another 11.8% planning to launch

- 61.2% of infused products are sold as multi-packs

- 68.4% of producers use internal infusion methods, primarily mixing flower and concentrate before packing

- Over half report infused products still account for less than 30% of their business

As noted, the top segment by revenue since 2023 has been the Infused segment, combining flower with a concentrate for a more potent, more flavorful and pricier pre-roll product.

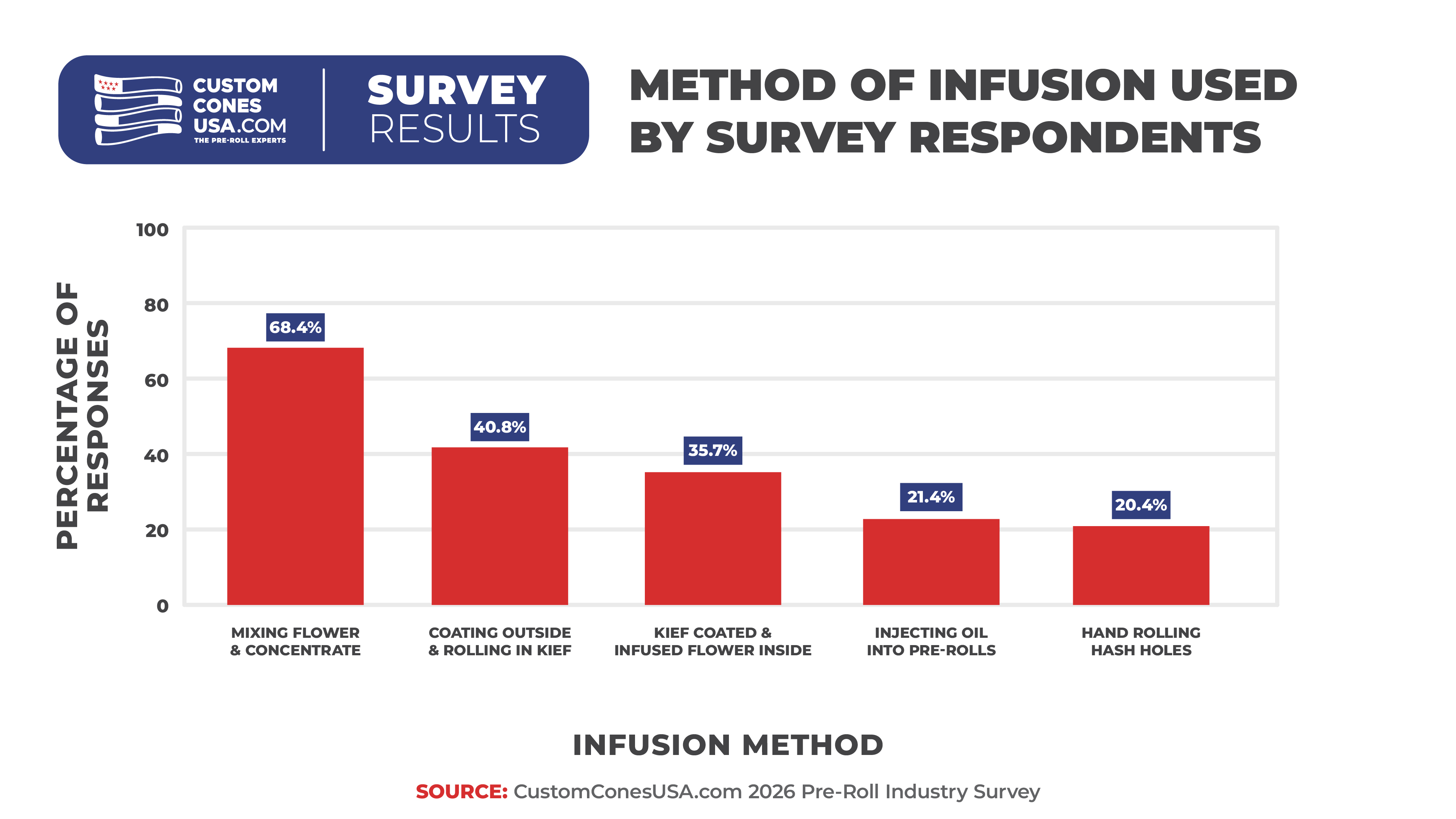

In our poll, 65.4% of respondents said they sell an infused product with another 11.8% planning to launch one. Of those that do, 61.2% sell infused multi-packs. Asked how they infuse their pre-rolls, 68.4% said they use an internal infusion method while only 8.2% use an external-only infusion method, such as kief dusting, and 23.5% use both.

More specifically, 68.4% mix their flower and concentrate prior to packing while 21.4% inject oil into their pre-rolls and 20.4% hand-roll hash hole-style pre-rolls. Another 35.7% combine kief and flower inside the cones while 40.8% coat the outside and rolling it in kief.

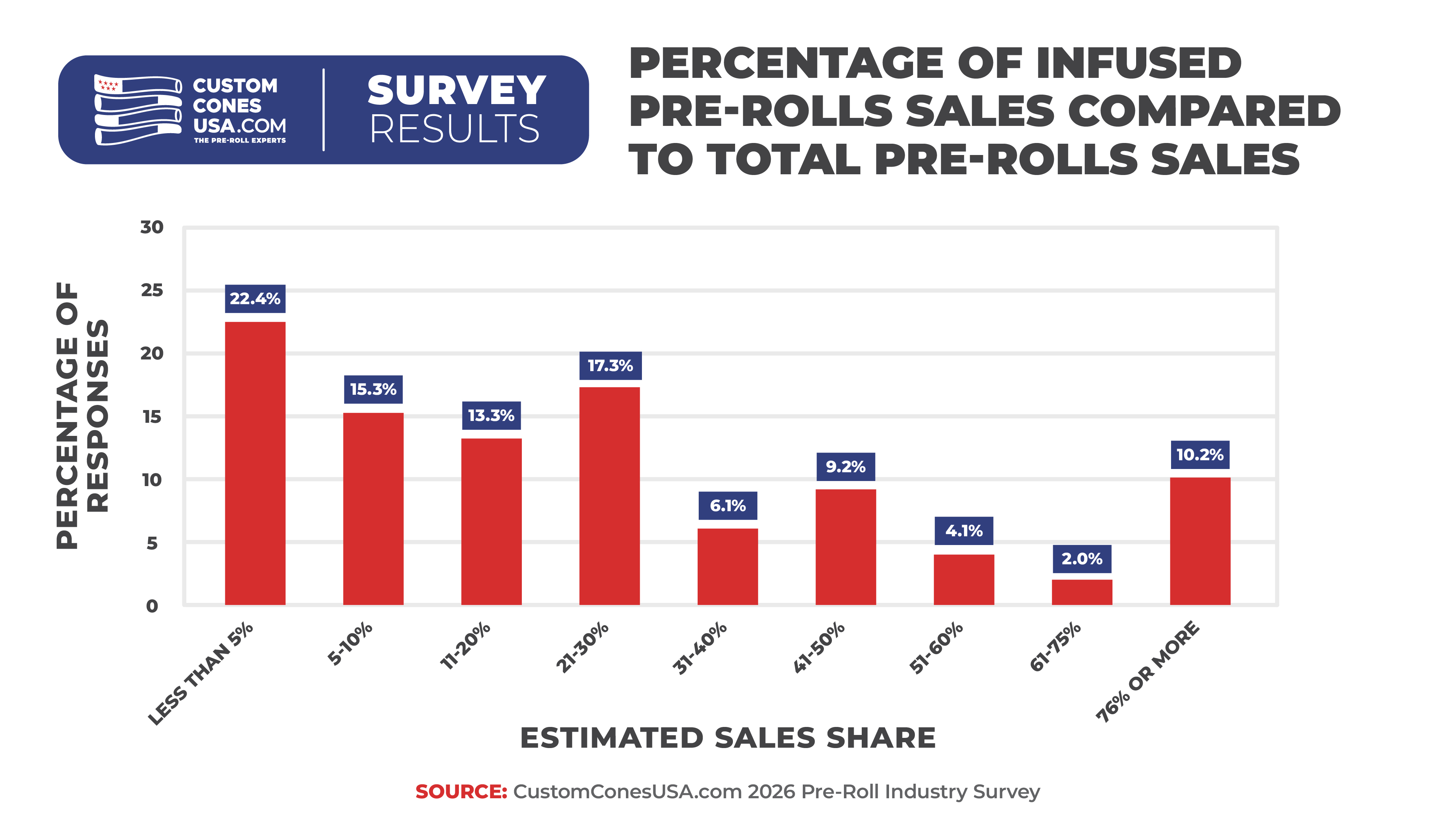

Interestingly though, for more than half of respondents (51%), infused pre-rolls still account for less than 30% of their business.

When we asked those that mix their flower and concentrate how they did it, 68.7% said they were still doing it by hand, while 7.5% were using a food mixer. Only 23.9% of respondents said they were using specialized machinery, such as the Infused Flower Mixer.

Use of Pre-Roll Machinery

Key Stats

- Industrial grinder usage rose to 44.9%, while handheld grinder use dropped to 22.1%

- 26% of producers still rely on basic grinding methods like blenders or shredders

- 63.8% use sifters to improve consistency, with additional adoption planned

As the industry matures, there are more and more machines designed to help with the filling of pre-rolled cones, speeding up and standardizing the processes. But what pre-roll machines are companies actually using and why?

As we know, high-quality pre-rolls always start with the grind, but not every grinder is equal. The choice of how you grind or shred your flower can drastically affect the quality of your pre-rolls. That’s because many whip-style grinders and shredders generate a lot of heat, which can damage the trichomes that house cannabinoids and terpenes, resulting in lower-potency, less-flavorful flower.

This year’s survey revealed that more companies are recognizing that reality and moving toward the Industrial Cannabis Grinder, which was built with pre-rolls in mind. The Industrial Grinder uses a high torque, low rpm motor to push the flower through screens, generating much less heat and protecting the trichomes.

In this year’s survey, 44.9% of respondents said they used the industrial grinder in their production facility, up from 34.4% in 2024. Handheld grinders saw the biggest drop, going from 34.4% usage in 2024 to 22.1% in 2026. Just over a quarter of producers (26%) still use basic machinery like blenders, food processors or shredders, despite the damage they can do to flower.

After grinding comes sifting, an often overlooked but crucial step in the creation of consistent, high-quality pre-rolls. Sifting helps guarantee consistent particle sizes that lead to better-packed pre-rolls and removes bits of stem and other jagged pieces that can tear pre-rolled cones during the packing process.

That’s why 63.8% of producers use a sifter, up from 59% in 2024, and another 9.5% are planning to use a sifter.

The Most Time-Consuming Steps in Pre-Roll Production

Key Stats

- Twisting and folding and cone loading tied as the most time-consuming steps at 24.4% each

- Filling issues are the leading cause of rework, cited by over 65% of respondents

- Time and labor remain the top operational frustration, followed by consistency challenges

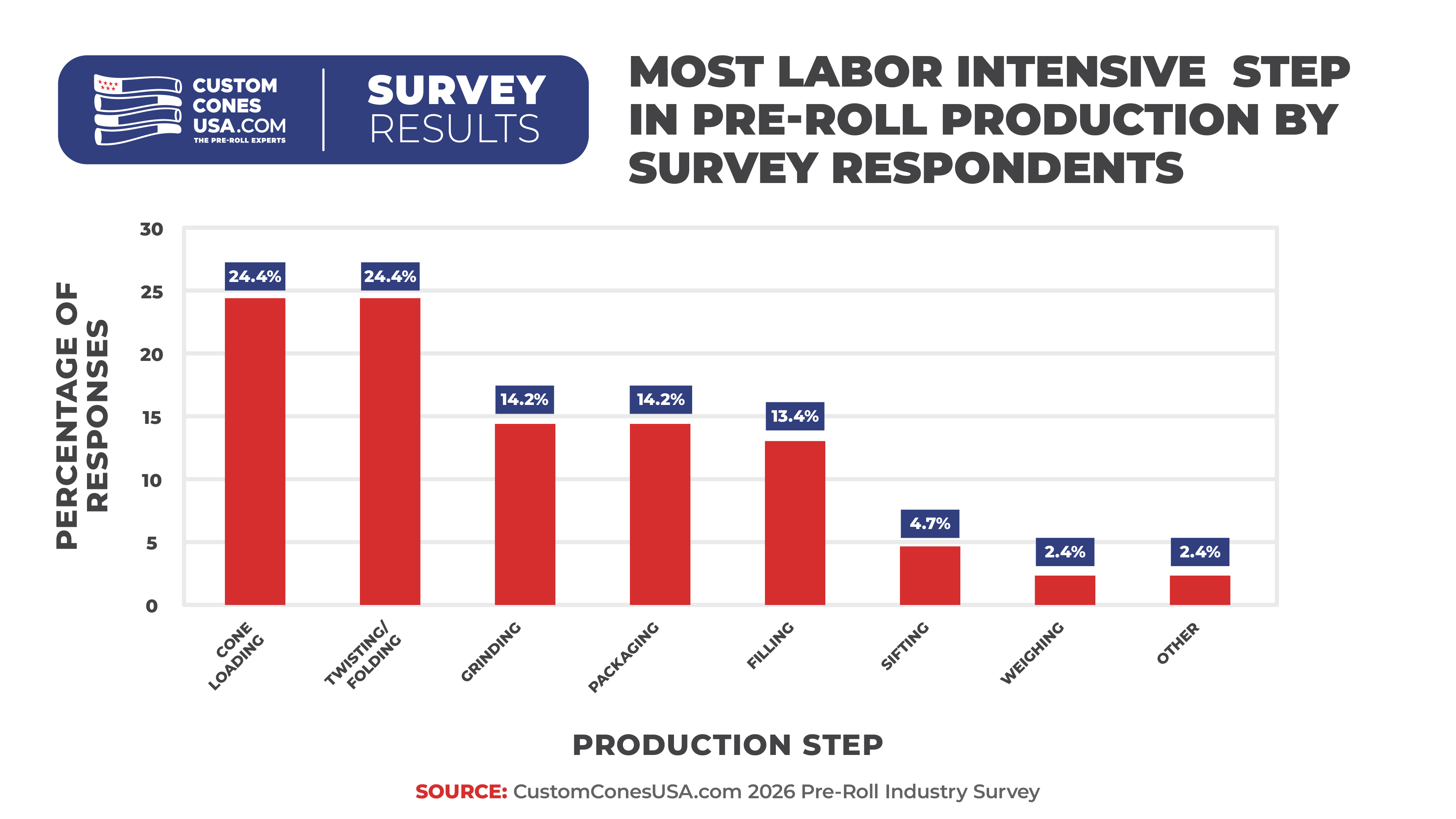

Traditionally, the most time-consuming part of pre-roll production has been closing cones, but this year, we have a tie at the top. While 24.4% of respondents said twisting/folding - the same percentage as in 2024 – it was joined this year with the same percentage saying “cone loading,” up from 22% in our last survey.

Several pre-roll machine manufacturers have looked to address these issues in the past few years, developing both closer tools and cone-loading devices that help ease both of these speed bumps.

“Grinding” and “Packaging” tied at 14.2% to come in second with “filling” landing next at 13.4%.

Interestingly enough though, when we asked what the top cause of re-work was, filling issues led the way with 32.7% saying “inconsistent fill weight” and another 32.7% saying “packed too tight or loose.”

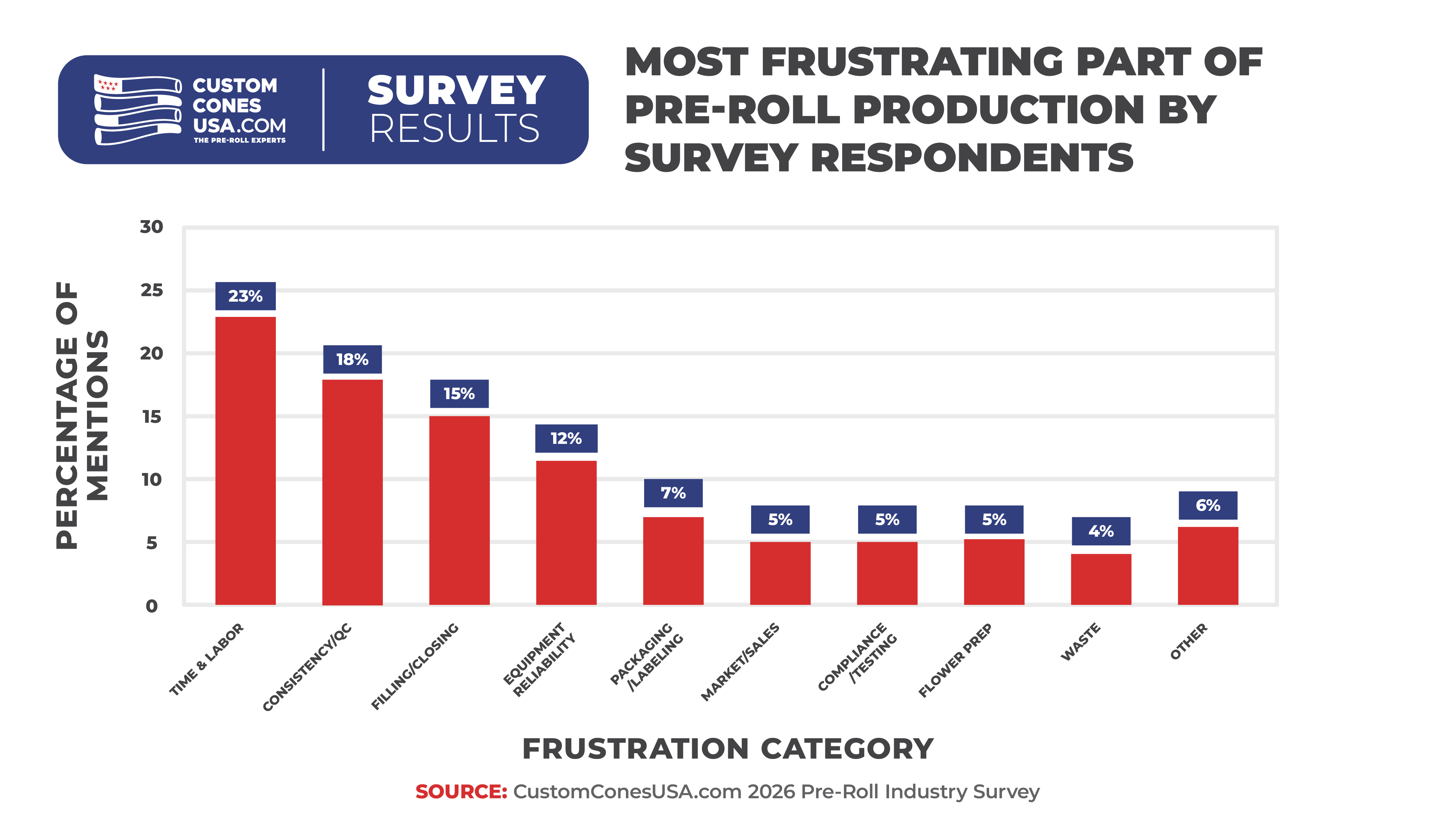

When asked directly what the most frustrating part of pre-roll manufacturing is, 28% mentioned time and labor, with 22% citing consistency and 18% saying filling/closing.

Responses from producers included:

- “bad inputs, supplier response time”

- “Consistency, labor cost”

- “The cost of the equipment”

- “Waiting on testing”

- “Moisture level consistency resulting in loading difficulty”

- “Time to weigh and close”

Employee PPE & Safety Equipment

The health and safety of employees that manufacture pre-rolls has been a major topic of discussion in the industry since a pre-roll worker died on the job in Massachusetts in 2023 and our survey results back that up.

This year, a full 94.5% of respondents said their employees use personal protective equipment during work hours, up from 85.8 in our previous survey. The most common (92.1%) PPE used in pre-roll production is gloves. Another 46.5% require hairnets and 43.3% use masks. Additionally, 37.8% said they use air filters in their facilities.

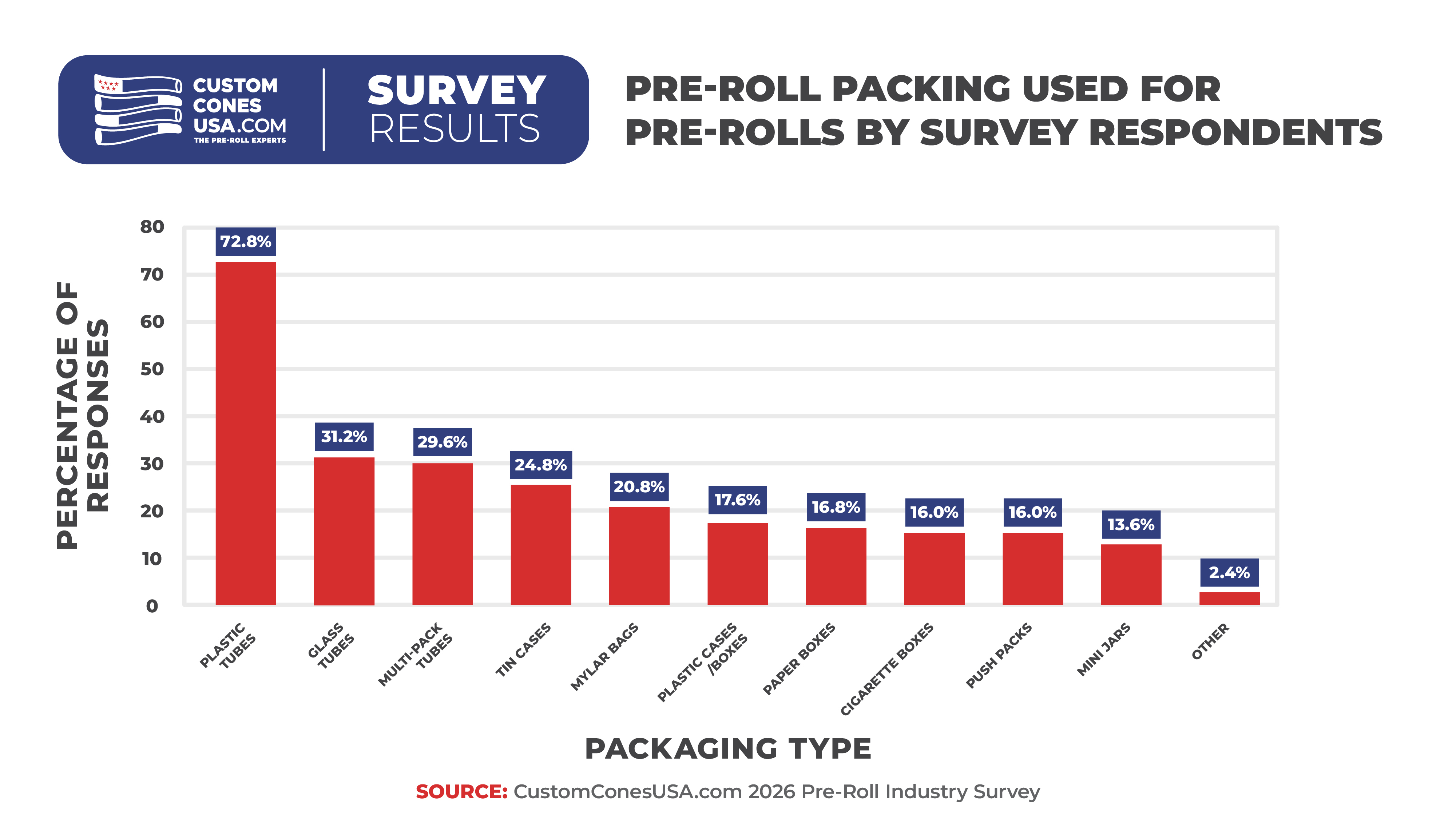

What Packing Options Do You Use?

Key Stats

- Pop-top packaging used by 70% of producers, with glass positioned as premium

While there are myriad packaging options for pre-roll manufacturers to choose from, we once again found that the plastic pop-top “doob tube” is by far the most popular, with 70.1% of respondents using them for at least some of their pre-roll products.

Glass Tubes come in a distant second with 34.7% choosing premium glass to highlight their pre-rolls.

What About Eco-Friendly Packaging?

Key Stats

- 75.6% of producers rate sustainable packaging importance at 5 or higher

- Average importance score dropped to 6.05, down from 6.9 previously

- 21.3% rate sustainability as extremely important

As noted, the majority of pre-roll manufacturers use plastic packaging for their products, most of which is not easily recyclable. We asked producers how important, on a scale of 1-10, it was to use recycled materials in their packaging.

While 21.3% chose “10” indicating it was very important, the overall average dropped to 6.05, down from 6.9 in our previous survey. Notably though, 75.6% of respondents gave the issue a “5” or higher, showing that pre-roll manufacturers are concerned about making environmentally conscious decisions.

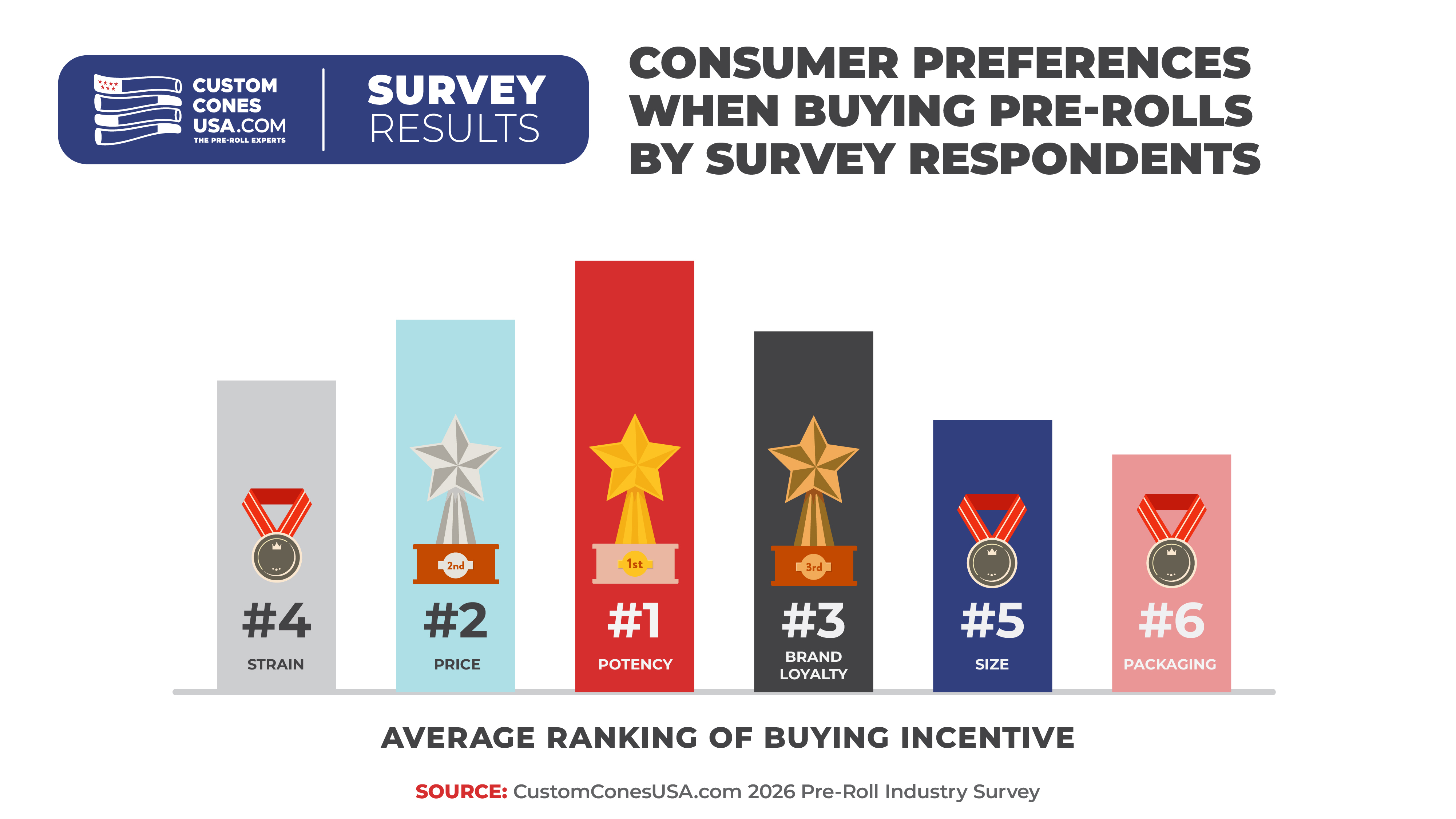

What Consumers Care About When Selecting Pre-Rolls

Key Stats

- Top purchase drivers are potency, price and brand, with brand rising to the third most important factor

- 59.8% of producers still use unbranded cones despite increasing brand importance

- All top pre-roll brands use custom filters or wraps to reinforce brand identity

- 60.6% of producers believe consumers consider filter type when purchasing

Our customer survey revealed that the top three things consumers look for when buying a pre-roll are potency, price and brand loyalty, and it appears that pre-roll manufacturers have heard them.

In our 2024 industry survey, producers correctly identified the top 2 spots as potency and price, but ranked brand loyalty all the way down at sixth, behind strain, paper type and packaging.

This year, companies have realized that like all consumer-packaged goods, brand is an important component of consumer choice and have ranked it accordingly, putting it in third place this year, just ahead of strain.

However, while producers now agree that brand is important, the majority of businesses (59.8%) in our survey still pack their pre-rolls in unbranded cones, leaving an opportunity for branding on the table.

In fact, all five of the Top 5 pre-roll brands in the country use custom-printed filters and/or external wraps on their pre-rolls, so customers know what brand they are smoking, even after the pre-roll comes out of its packaging.

We also asked producers if they believed customers care about the filter type on their pre-rolls, such as paper spirals, wood, glass or premium ceramic filter tips, and 60.6% agreed that consumers do consider filter tips when making a pre-roll purchase.

What's Next for Pre-Rolls

Key Stats

- Key trends include infused growth, price compression and premium product formats

- Top risks include oversupply (52.8%) and regulatory uncertainty

- 47.5% of operators report using AI in their business

The pre-roll segment thrives on innovation and change so we asked producers what they saw as the next big trend in the cannabis industry.

The most common answer involved infused pre-rolls, followed by pre-rolls in general continuing to grow as a category. Producers also see price compression/lower prices continuing into the future.

Several are also predicting further states legalizing and premium or specialty formats becoming more important to the segment and industry as a whole.

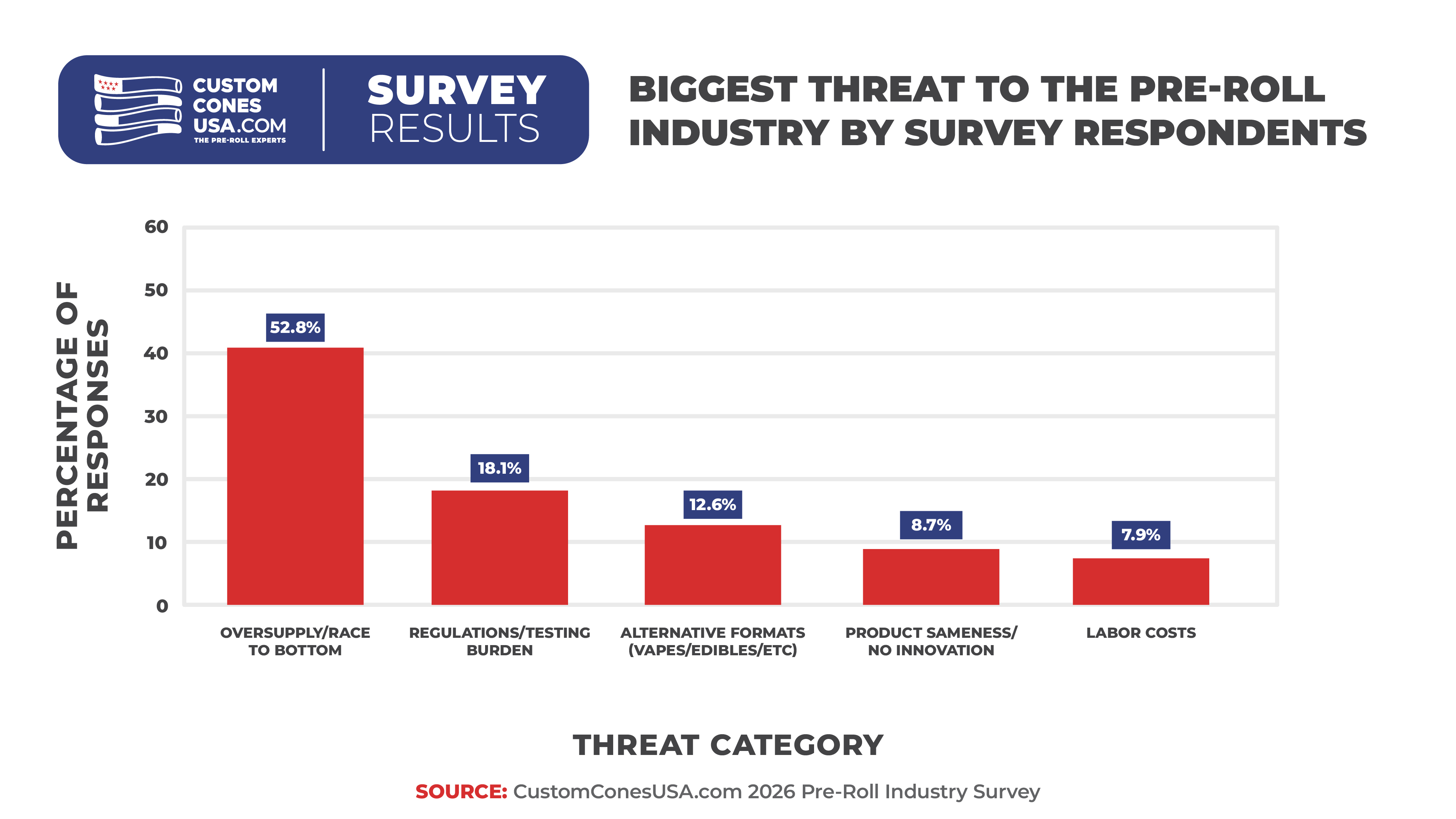

What Is the Biggest Threat to Pre-Rolls?

On the other side, we asked what producers perceived as the biggest threat, and a full 52.8% of respondents said they were concerned about oversupply and the “race to the bottom” for pricing. Another 18.1% are concerned about regulations and testing while 12.6% worry about other formats, such as vapes or edibles.

Pre-Rolls & AI

Finally, tackling one of the top business concerns of the nation, we asked pre-roll manufacturers if they were using artificial intelligence at all as part of their business. And while a majority still do not use AI, the results were closer than expected, with 47.5% saying that is part of their workflow.

The State of the Pre-Roll Market in 2026 and Beyond

Key Stats

- Pre-rolls are the fastest-growing major cannabis category and lead in unit sales

- Growth is driven by infused products, multi-pack formats and price accessibility

- Competitive advantage depends on balancing price, potency, consistency and branding

Even with five years of consistent growth that outperformed the industry as a whole, pre-rolls remain the fastest-growing major category in terms of revenue and this year topped flower as the top-selling product in terms of unit sales.

The Pre-Roll category is strong and is only getting stronger. Characterized by innovation and adaptation, our analysis once again shows a sector of the industry driven by and meeting consumer demand for new, interesting and potent products, all at a price point that encourages experimentation.

Expansion into new markets and growth in maturing markets will bring continued growth in 2026 and beyond, with new machines and innovations – such as mixers, closers and cone-loading devices – that help producers meet demand while continuing to drive down both costs and prices.

As the pre-roll category matures, success will hinge on consistency, freshness of product and branding that separates the premium pre-roll products from those that get left behind.

By combining potency with price point and innovative sizes and forms, we see the pre-roll category continuing to drive the entire industry forward in the foreseeable future, not just surviving, but thriving to shape the future of the entire cannabis industry.

Brian Beckley spent 20 years as an award-winning newspaper journalist and editor, covering cities on both coasts before becoming Managing Editor of Marijuana Venture magazine, where he covered all aspects of the cannabis industry for five years. In his role with the magazine, he spoke at numerous cannabis conferences and hosted several media panels. Brian joined Custom Cones USA and DaySavers as lead copywriter & editorial strategist in 2023.

Our annual State of the Pre-Roll Market Report reviews 2025 in pre-rolls, and what the future holds for the category.