Pre-Roll Prices: The Pre-Roll Pricing Cycle

Posted by Custom Cones USA on May 8th 2024

There are few more recognizable symbols of cannabis legalization than the humble pre-roll, the fastest-growing segment of the cannabis market for several years now. And as the numbers from the first part of 2024 show, the product’s popularity continues to grow, climbing to 15% of the market share in April.

One of the reasons the pre-roll continues to grow in popularity is, of course, the ease and portability of the product itself, but also the price point, which makes it an easy add-on at every dispensary in the country. In April, the average price of the more than 94.5 million pre-rolls sold across the states tracked by cannabis analytics firm Headset is down to $6.73. Pre-roll prices averaged $8.03 in April 2023, a 16% drop year-over-year.

The overall average consumer price of a pre-roll is down due to the drop of material costs in maturing markets, even as the continued growth in the higher-priced infused, or connoisseur, sector continues to drive the entire segment with a 27.9% year-over-year growth through the first four months of 2024.

But drilling deeper into the data reveals wildly inconsistent pricing and sales across the legal states, with Michigan currently standing as the undisputed king of the pre-roll market in sales.

The data also points to the cycle of pricing that occurs as markets mature, providing a bit of a road map of what to expect pricewise for producers in states that have recently opened recreational markets.

Michigan vs. Pre-Rolls

No state sells more pre-rolls than Michigan, which began recreational sales in 2019. In fact, no other state even comes close.

Headset data for part of this year indicates that consumers in The Great Lake State bought a whopping 22.7 million pre-rolls so far this year, dwarfing the second-highest sales total of 12.6 million in the much larger and more mature market of California.

That might have something to do with the price. According to Headset, Michigan pre-rolls have an average, equalized cost of $6.39 per gram, down from $8.30 at the same time in 2023, a decrease of 23%. Michigan also has the second-lowest infused pre-roll average price in the country at $10.23.

In fact, a deeper dive into the data shows that 88% of pre-roll products sold in Michigan are priced below the $10 mark – the highest percentage in the country – and more than half (51%) are less than $5.

Only Washington state residents pay less for their pre-rolls ($6.19) and infused pre-rolls ($6.34).

Meanwhile, in New York Pre-Rolls

At the other end of the spectrum is New York, where that state’s stunted roll-out is keeping prices high and sales low..

While the New York legislature passed a legalization measure in 2021, the state’s recreational market is still mostly nascent with the vast majority of licenses yet to be released. Still, the state’s first recreational sales began in late 2022 at a limited number of retail stores.

But because it is still in the early stages of its legalization cycle, demand and price points remain high, resulting in an average pre-roll price of $24.81 with infused pre-rolls commanding a whopping $30.75, both the highest in the nation by more than $5.

And with prices like that, it’s little surprise that only 640,000 pre-rolls were sold in the Empire State across the first part of 2024. No other state sold fewer than 1.9 million (Maryland).

But New York remains an outlier, as even the country’s newest markets, Maryland and Missouri, show strong pre-roll sales growth and price points favorable to consumers.

Legacy Market Pre-Rolls

As recreational markets mature, pre-roll sales and pricing often follow a familiar pattern. Because getting flower to market is often the most important consideration when states begin opening cannabis retail stores, pre-rolls can be something of an afterthought, rarely being made with the best flower.

But as growers get more sophisticated and more licenses are issued, more flower becomes available for pre-rolls, making them a more desirable item. As growers produce even more, extraction becomes a more attractive option leading to a rise in infused products, including pre-rolls, driving prices down across the board as supply rises to meet demand.

The cycle can be seen in the price points of pre-rolled products in legacy markets compared to the prices of those in new markets. The three oldest recreational markets – Colorado (stores opened in 2014), Washington (also 2014) and Oregon (2015) – for example, have three of the four lowest prices on pre-rolls in the country (with Michigan being the other).

As noted, Washington residents pay the lowest price in the country at an average of $6.19 and $6.34 for infused pre-rolls. In total, 87% of all pre-roll products in the Evergreen State are priced below $10. And with prices like that, it’s no surprise that Washington retailers sold 7.3 million pre-roll products in the first part of 2024, good enough for the fourth-most sold in the country, despite the state ranking only 13th in population.

Though Michigan slides in at the second-lowest price, Oregon follows at third with an average pre-roll price of $7.51, which, surprisingly, is slightly up from the same time in 2023 and likely due to sales of infused products ($9.05) and mixed strain product that clocks in at $17.64, driving up the average. Overall, 73% of pre-rolls are priced at less than $10, leading to Oregon ranking sixth in pre-rolls sold at 4.1 million items, pretty good for a state ranking 27th in population.

Colorado follows in fourth with an average pre-roll price of $7.98 - up from $7.75 last year – and an infused average of $14.88. About 80% of pre-roll products are priced below $10 and the state ranks seventh among the Headset data with 4.3 million pre-rolls sold so far this year.

Pre-Rolls in Developing Markets

Following the initial wave of legalization in Colorado, Washington and Oregon, several other states launched regulated adult-use programs of their own with Nevada opening its market in 2017 and Massachusetts and California following in 2018.

Those states, interestingly enough, constitute the majority of the next tier in Headset’s price point data. Each of these states is at the part of the cycle where they are producing enough flower to see an increase in quality and drop in price of pre-roll products, but still see high prices on infused pre-rolls because they have not yet reached full maturity.

Arizona, which opened its recreational market in 2021, also sneaks into this level, but the transition to recreational in that state was unusually smooth. The state had a thriving medical market in place since 2012 and medical dispensaries were simply opened to the public only a few months after voters approved adult use in November 2020, the fastest rollout in the industry.

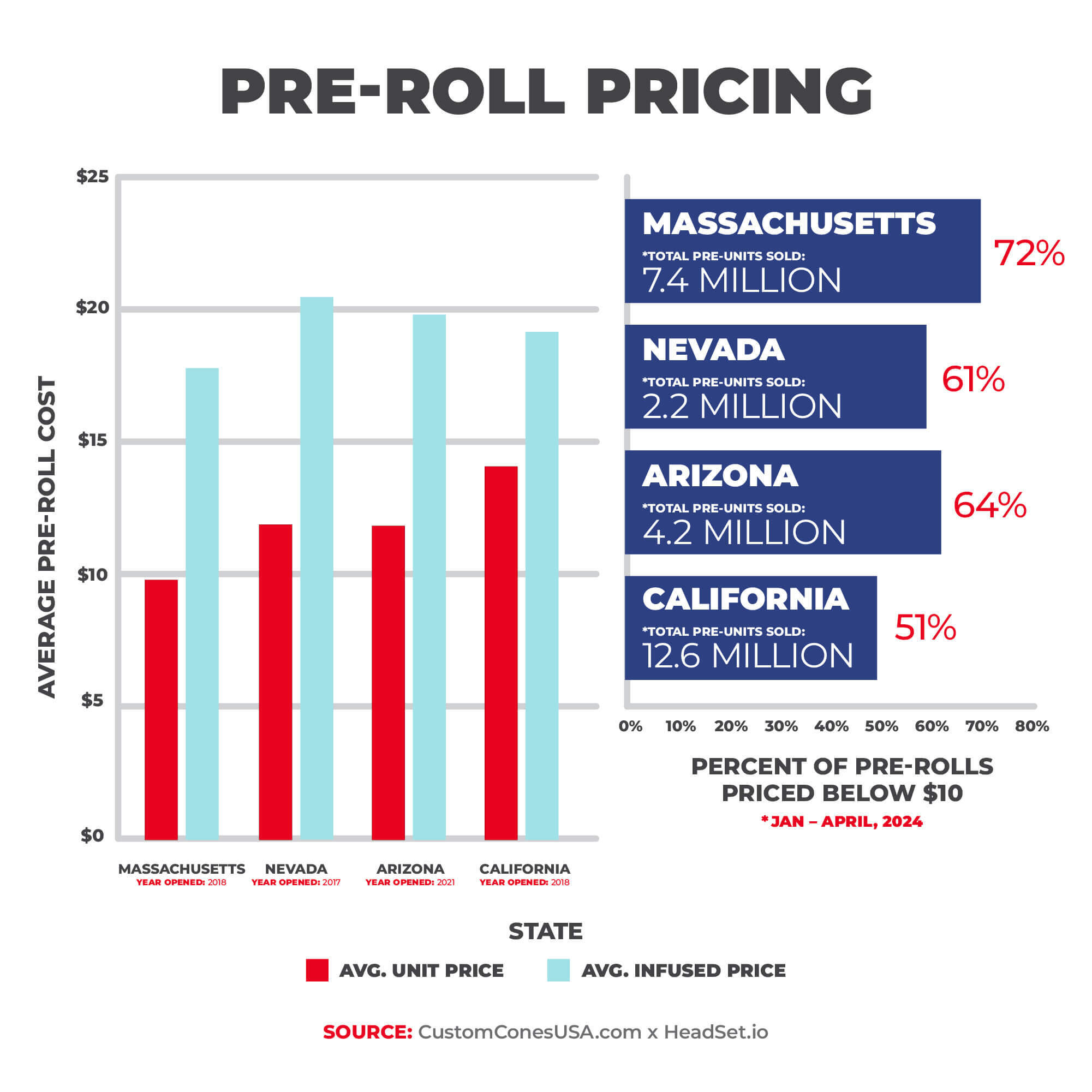

At an average pre-roll price of $9.83, Massachusetts comes in fifth among the data. But true to its middle-era nature, while 72% of pre-rolls are priced below $10, infused pre-rolls in the Bay State climb to an average of $17.38. That said, Massachusetts still ranks fourth in the number of products sold with 7.4 million pre-rolls flying out of dispensaries.

Arizona slides in sixth with an average pre-roll price point of $11.87 (down from $13.36 in 2023), the first state with an average price above $10, though a full 64% of pre-rolls arepriced at less. Infused pre-rolls still run at an average of $19.20, however, bringing up the overall average price. All told, Arizona is good enough for the fifth among tracked states with 4.2 million pre-roll products sold so far this year.

In seventh is Nevada, with an average price of $11.92, with 61% of pre-rolls coming in at less than $10. Nevada’s overall average, however, like other states at this tier, is driven up by the price of infused products, which sit at an average of $20.50 each. Overall, the state ranks ninth in pre-roll sales at 2.2 million units sold.

In eighth place, we have finally reached the largest legal cannabis market in the country: California. Despite ranking first in population, California comes in second in sales at 12.6 million items sold (more than 10 million behind Michigan) and has an average price point of $14.11, with infused items jumping to an average of $19.20. Still, a full 51% of California pre-roll products are priced at less than $10.

Emerging Market Pre-Roll Prices

The final tier of prices among the data sees another jump in average cost among the newest states to open their recreational markets. Illinois, Missouri, Maryland and New York have all launched sales since 2020 and their pre-roll prices reflect markets still trying to meet demand.

At an average of $14.48, Missouri is the lowest among this final tier of states, though infused pre-rolls average $19.95 each. Unsurprisingly, only 44% of pre-roll products are priced below $10. That has not stopped sales, however, as Show Me State consumers have purchased 2.5 million pre-roll products so far this year, pretty good for a market that opened in 2023.

Also opening in 2023, Maryland comes in close behind with an average price of $14.84 and an infused average of $23.13. Only 27% of pre-roll products in this emerging market are priced less than $10, resulting in a total of 1.9 million pre-rolls sold so far this year.

Next up is Illinois, which opened its recreational market in 2020. Despite a head start on other states, Illinois still has a remarkably high average price of $19.24 and an infused average of $24.67. Only 21% of products are cheaper than $10, though Illinois retailers still moved 2.6 million pre-roll units.

And, as mentioned, New York brings up the rear with the highest pre-roll prices among the ranked states, with an average of $24.81 and an infused average price of more than $30. However, with a massive population and the vast majority of licenses yet to be issued, prices in the Empire State should not remain this high for very long, assuming state regulators complete their work and fully open the market.

Final Thoughts

Pre-rolls remain the fastest growing sector of the cannabis economy and the No. 1 add-on at dispensaries because of their ease, portability and price point, all of which allow for experimentation by consumers. But pre-roll prices in markets around the country follow a predictable cycle as they mature, and producers/processors ramp up to meet demand and the most recent Headset data bear that out.

With Michigan, of course, being the exception that proves the rule.

So whatever market you are in, it is important to prepare for the next stage of pricing and customer expectations to remain competitive and stand out among the multitude of pre-roll brands appearing on dispensary shelves.

Contact the Pre-Roll experts today to see how to prepare your pre-roll line for the next step and how to ensure that your brand dominates this exciting and growing market.

There are few more recognizable symbols of cannabis legalization than the humble pre-roll, the fastest-growing segment of the cannabis market for several years now. And as the numbers from the first part of 2024 show, the product’s popularity continues to grow, climbing to 15% of the market share in April.